Liquid Death’s rise on Amazon is hard to ignore. Over the past two years, sales are up +172%, and the brand keeps feeding the flywheel with new flavor launches. Even the spicy one is legitimately good, which is not something people usually say about “spicy water.”

But the bigger story is what the leaderboard reveals about the entire category: carbonated water on Amazon is basically a bulk-buy game. It’s starting to look less like a “search and discover” channel and more like a Costco-style pantry restock loop.

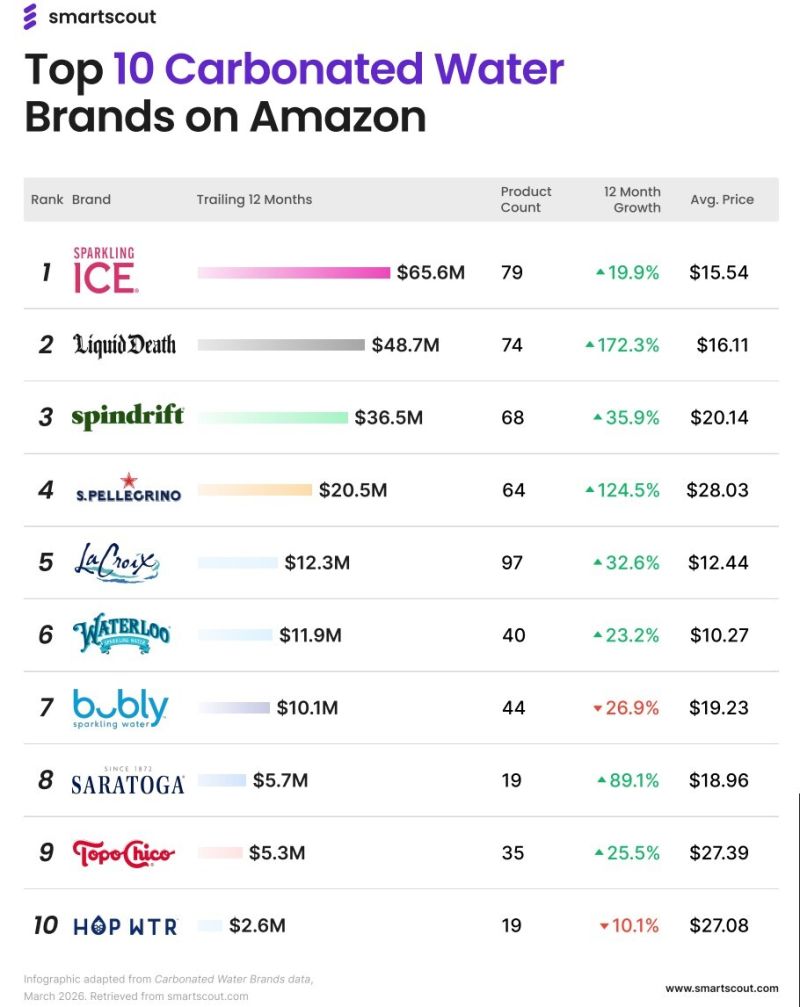

Top 10 Carbonated Water Brands on Amazon (TTM)

(SmartScout estimates, trailing 12 months)

Rank

Brand

Est. Yearly Revenue (TTM)

12 Month Growth

1

Sparkling Ice

$65.6M

+19.9%

2

Liquid Death

$48.7M

+172.3%

3

Spindrift

$36.5M

+35.9%

4

S.Pellegrino

$20.5M

+124.5%

5

LaCroix

$12.3M

+32.6%

6

Waterloo

$11.9M

+23.2%

7

bubly

$10.1M

−26.9%

8

Saratoga

$5.7M

+89.1%

9

Topo Chico

$5.3M

+25.5%

10

HOP WTR

$2.6M

−10.1%

What stands out (and why it matters)

1) Every brand here is 1P

That’s the loudest signal in the dataset.

Beverages are heavy, low margin, and operationally unforgiving. The “best” business model on Amazon is often the one with:

the cheapest landed freight

the most consistent in-stock position

the best ability to run promos and hold the Buy Box

the lowest cost per unit to ship and handle

That’s a 1P advantage most of the time.

2) Liquid Death is building a brand moat

Most water brands fight on price-per-can and flavor variety.

Liquid Death fights on identity. The packaging is a billboard. The name is polarizing. The vibe is meme-ready. It turns a commodity product into something people talk about, gift, and share.

That creates real insulation against “another 12-pack is $2 cheaper.”

3) Legacy brands aren’t dead

S.Pellegrino growing triple digits is a reminder that “old brand” does not mean “stagnant brand.”

Amazon isn’t only a disruptor channel. For the right products, it’s also a distribution accelerator for brands that already have trust.

4) Not all boats are rising

bubly is down −26.9% and HOP WTR is down −10.1%. That usually happens in categories where:

price competition intensifies

pack economics change

promotions become more aggressive

or the brand loses momentum in visibility (ads + ranking + reviews + availability)

Is it possible to do beverages as a 3P seller?

Yes, but it’s hard to do at scale and even harder to dominate.

Where 3P typically struggles in beverages:

Shipping economics: water is heavy; shipping kills profit if your cost structure is off by a little

Damage/returns: dented cans, leaking cases, and customer dissatisfaction compound fast

Pricing wars: 1P can often sustain lower pricing and still win the Buy Box consistently

So yes, it’s possible. But the leaderboard tells you it’s not the default path.

Amazon is quietly a Costco competitor

This is the most underrated takeaway. People aren’t shopping carbonated water like they shop gadgets. They’re restocking. That behavior is closer to warehouse club shopping than traditional Amazon browsing.

And that shifts what “winning” looks like:

bigger packs

predictable replenishment

dependable availability

competitive per-unit pricing

“I have to imagine profit margins here are low.” You’re probably right.

But here’s what you might be missing:

Brands may accept lower margin for velocity. High-volume pantry staples can be a strategic channel, not a profit-max channel.

The customer lifetime value can be strong. If you become the default restock, you don’t need to “win discovery” every time.

Promo + Subscribe & Save can drive stability. It’s less about one-time impulse and more about repeat behavior.

Amazon rewards conversion and consistency. In-stock and Buy Box consistency can matter more than branding.

The real question

Liquid Death is proving that branding still matters in a commodity category. But the leaderboard also proves that distribution mechanics matter even more.

So the question isn’t just “who has the best water.” It’s: who can win the restock loop without bleeding out on logistics.

Liquid Death’s rise on Amazon is hard to ignore. Over the past two years, sales are up +172%, and the brand keeps feeding the flywheel with new flavor launches. Even the spicy one is legitimately good, which is not something people usually say about “spicy water.”

But the bigger story is what the leaderboard reveals about the entire category: carbonated water on Amazon is basically a bulk-buy game. It’s starting to look less like a “search and discover” channel and more like a Costco-style pantry restock loop.

Top 10 Carbonated Water Brands on Amazon (TTM)

(SmartScout estimates, trailing 12 months)

Rank

Brand

Est. Yearly Revenue (TTM)

12 Month Growth

1

Sparkling Ice

$65.6M

+19.9%

2

Liquid Death

$48.7M

+172.3%

3

Spindrift

$36.5M

+35.9%

4

S.Pellegrino

$20.5M

+124.5%

5

LaCroix

$12.3M

+32.6%

6

Waterloo

$11.9M

+23.2%

7

bubly

$10.1M

−26.9%

8

Saratoga

$5.7M

+89.1%

9

Topo Chico

$5.3M

+25.5%

10

HOP WTR

$2.6M

−10.1%

What stands out (and why it matters)

1) Every brand here is 1P

That’s the loudest signal in the dataset.

Beverages are heavy, low margin, and operationally unforgiving. The “best” business model on Amazon is often the one with:

the cheapest landed freight

the most consistent in-stock position

the best ability to run promos and hold the Buy Box

the lowest cost per unit to ship and handle

That’s a 1P advantage most of the time.

2) Liquid Death is building a brand moat

Most water brands fight on price-per-can and flavor variety.

Liquid Death fights on identity. The packaging is a billboard. The name is polarizing. The vibe is meme-ready. It turns a commodity product into something people talk about, gift, and share.

That creates real insulation against “another 12-pack is $2 cheaper.”

3) Legacy brands aren’t dead

S.Pellegrino growing triple digits is a reminder that “old brand” does not mean “stagnant brand.”

Amazon isn’t only a disruptor channel. For the right products, it’s also a distribution accelerator for brands that already have trust.

4) Not all boats are rising

bubly is down −26.9% and HOP WTR is down −10.1%. That usually happens in categories where:

price competition intensifies

pack economics change

promotions become more aggressive

or the brand loses momentum in visibility (ads + ranking + reviews + availability)

Is it possible to do beverages as a 3P seller?

Yes, but it’s hard to do at scale and even harder to dominate.

Where 3P typically struggles in beverages:

Shipping economics: water is heavy; shipping kills profit if your cost structure is off by a little

Damage/returns: dented cans, leaking cases, and customer dissatisfaction compound fast

Pricing wars: 1P can often sustain lower pricing and still win the Buy Box consistently

So yes, it’s possible. But the leaderboard tells you it’s not the default path.

Amazon is quietly a Costco competitor

This is the most underrated takeaway. People aren’t shopping carbonated water like they shop gadgets. They’re restocking. That behavior is closer to warehouse club shopping than traditional Amazon browsing.

And that shifts what “winning” looks like:

bigger packs

predictable replenishment

dependable availability

competitive per-unit pricing

“I have to imagine profit margins here are low.” You’re probably right.

But here’s what you might be missing:

Brands may accept lower margin for velocity. High-volume pantry staples can be a strategic channel, not a profit-max channel.

The customer lifetime value can be strong. If you become the default restock, you don’t need to “win discovery” every time.

Promo + Subscribe & Save can drive stability. It’s less about one-time impulse and more about repeat behavior.

Amazon rewards conversion and consistency. In-stock and Buy Box consistency can matter more than branding.

The real question

Liquid Death is proving that branding still matters in a commodity category. But the leaderboard also proves that distribution mechanics matter even more.

So the question isn’t just “who has the best water.” It’s: who can win the restock loop without bleeding out on logistics.

The Helium 10 vs. Jungle Scout debate has remained relevant for more than a decade.

These two platforms have dominated the Amazon seller tool space since 2015, and nearly every FBA seller has used one or both at some point. But the question that keeps coming up in every Amazon seller community, subreddit, and Facebook group is the same: which one should you actually pay for?

Both tools have changed significantly in 2026. Helium 10 removed its affordable Starter plan, raised prices across the board, and expanded into Walmart and TikTok Shop. Jungle Scout rebranded its entire plan structure under the "Catalyst" name, refined its AI tools, and doubled down on what it has always done well: helping sellers find and launch products on Amazon.

Both platforms look similar on the surface. They're not. Here's exactly where they differ and which one is worth your money in 2026.

Helium 10 vs Jungle Scout: Quick Verdict

Jungle Scout Catalyst is the better choice for beginners, budget-conscious sellers, and anyone focused on product research and validation. Its simplified workflows, superior supplier database, and lower pricing make it the smarter entry point into Amazon selling.

Helium 10 is the better choice for experienced sellers who need advanced keyword research, PPC automation, and multi-channel selling across Amazon, Walmart, and TikTok Shop. Its tool depth is unmatched, but the pricing reflects that.

That said, both tools share a common gap: neither provides brand-level market intelligence, subcategory revenue analysis, or seller mapping. Sellers who need that strategic market view often pair Helium 10 or Jungle Scout with a dedicated market intelligence platform like SmartScout, using it to identify opportunities at the brand, category, and seller level before moving into product research and optimization.

Here is a side-by-side snapshot of how both tools stack up across every major capability. Pay attention to the three rows near the bottom (Brand Intelligence, Traffic Analysis, Seller Mapping), as they highlight where both platforms have blind spots.

Parameter

Helium 10

Jungle Scout Catalyst

Specialization

All-in-one seller suite with 20+ tools

Beginner-friendly product research and launch platform

Best For

Experienced sellers and scaling operations

New sellers, SMBs, and product validation

Product Research

Black Box with advanced filters

Product Database and Opportunity Finder

Keyword Research

Cerebro and Magnet with deep ASIN-level data

Keyword Scout with simpler, actionable insights

Listing Optimization

Scribbles and AI Listing Builder with ChatGPT

Listing Builder with AI Assist

PPC Management

Adtomic with full automation and AI-driven campaign support

Advertising Analytics through Growth Accelerator+

Supplier Sourcing

Supplier Finder through Alibaba via Chrome extension

Supplier Database with global, vetted suppliers and shipment data

Review Automation

No built-in tool

Yes, through Growth Accelerator+

Rank Tracking

Up to 2,500 keywords per product with daily updates

Rank Tracker with relevancy scoring

Inventory Management

Yes, through the Diamond plan

Inventory Manager through Growth Accelerator+

Chrome Extension

Xray, paid and Chrome only

Free extension for Chrome and Firefox

Brand Intelligence

Market Tracker at the product level

No brand-level analytics

Traffic Analysis

No equivalent

No equivalent

Seller Mapping

No equivalent

No equivalent

AI Tools

AI chat, listing builder, and PPC automation

AI Assist for chat, listings, review analysis, and analytics

Free Trial

Free plan with limited access

7-day money-back guarantee

Starting Price

$129/month for the Platinum plan

$49/month for the Starter plan

Trustpilot Rating

2.3/5 from 700+ reviews

4.2/5 from 3,900+ reviews

The table makes one thing clear: these tools overlap in many areas but differ sharply in philosophy. Helium 10 goes wide and deep. Jungle Scout keeps things focused and accessible. And both leave market-level intelligence off the table entirely.

Who Should Choose Helium 10?

Go with Helium 10 if:

You already have an established Amazon business and want advanced optimization tools

You sell on Walmart or TikTok Shop in addition to Amazon

You want granular keyword data with Cerebro's IQ Score and advanced filtering

You need full PPC campaign automation, not just analytics

You manage multiple seller accounts and need the Diamond plan's multi-user access

Skip Helium 10 if:

You are launching your first product and want a guided workflow

You are on a tight budget (no plan under $129/month)

You need a built-in supplier database for sourcing products

You find 20+ tools overwhelming and prefer a streamlined interface

You want brand-level competitive intelligence or seller mapping (consider SmartScout instead)

Who Should Choose Jungle Scout?

Go with Jungle Scout if:

You are a new Amazon seller learning the ropes

You want product research, supplier sourcing, and listing tools in one affordable package

You run a small-to-medium business and need solid data without enterprise complexity

You want automated review requests built into your plan

You prefer a clean, intuitive interface with a shorter learning curve

Skip Jungle Scout if:

You sell on Walmart or TikTok Shop (Jungle Scout is Amazon-only)

You need advanced PPC bid automation and campaign management

You want the deepest possible keyword research with ASIN-level reverse lookups

You need to analyze entire brand ecosystems and wholesale opportunities

Helium 10 vs Jungle Scout: Platform Overviews

Helium 10 and Jungle Scout have been the biggest competitors against each other for the last decade. Millions of seller trust both tools for their capabilities. Let’s know more about them.

Helium 10 Overview

Helium 10 launched in 2015 as a Chrome extension built by Manny Coats and Guillermo Puyol. The idea was simple: give Amazon sellers the most accurate marketplace data available. Over the years, it expanded into a massive suite of 20+ integrated tools covering product research, keyword analysis, listing creation, PPC management, inventory tracking, and refund recovery.

In 2026, Helium 10 made two significant moves. First, it retired the $39 to $49 Starter plan, making Platinum ($129/month) the cheapest paid option. Second, it expanded beyond Amazon with full Walmart marketplace support and TikTok Shop tools, including a listing converter, influencer finder, and profitability calculator. The platform now positions itself as a multi-channel e-commerce toolkit rather than a pure Amazon tool.

Training comes via the Freedom Ticket course by Kevin King, included free with every paid plan. The course is regularly updated and remains one of the most comprehensive Amazon FBA training programs available.

Related: See how Helium 10 compares to SmartScout's market intelligence in our SmartScout vs Helium 10 comparison.

Jungle Scout Overview

Jungle Scout also launched in 2015, founded by Greg Mercer after his early experience selling supplements on Amazon. The platform started with a singular focus: helping sellers find profitable products to sell. That DNA still runs through everything Jungle Scout builds.

In 2026, Jungle Scout rebranded its seller plans under the "Catalyst" umbrella. The old Basic, Suite, and Professional tiers are now Starter ($49/month), Growth Accelerator ($79/month), and Brand Owner ($149/month). For enterprise brands doing over $5 million annually, Jungle Scout offers Cobalt, a separate competitive intelligence platform with custom pricing.

Jungle Scout tracks over 600 million ASINs and uses 11 years of refined sales estimation algorithms. The AI Assist feature now spans four areas: sales analytics, review analysis, listing building, and an always-on Q&A chat. The Jungle Scout Academy provides free training modules for every plan.

Helium 10 vs Jungle Scout: Feature-by-Feature Comparison

Both tools promise to help you sell more on Amazon. But their approaches differ in meaningful ways. Here is how they compare across every feature that actually matters to your bottom line.

1. Product Research

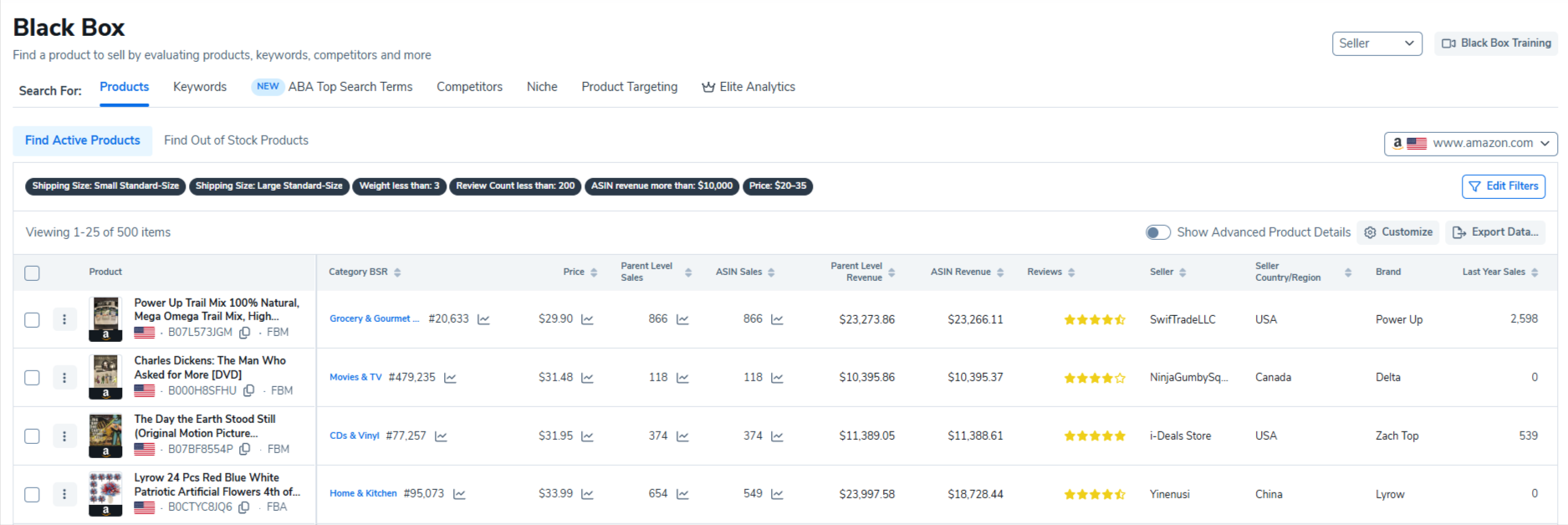

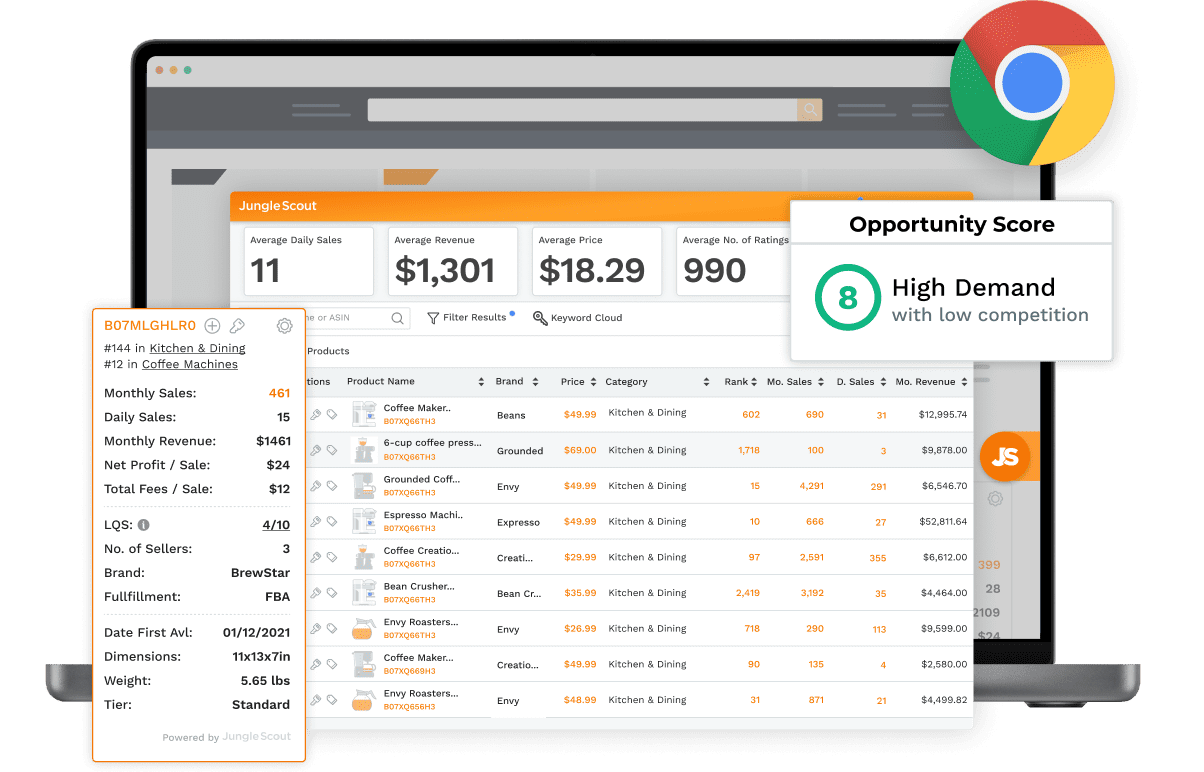

Helium 10: Black Box

Black Box is Helium 10's primary product research tool. It uses advanced filters, including price range, monthly revenue, review count, weight, category, and BSR to generate a list of product opportunities. The filters are highly configurable, and experienced sellers can create very specific search criteria to uncover niche products.

One advantage of Black Box is its integration with the broader Helium 10 suite. You can run a product search, click through to Cerebro for keyword analysis, and then move directly into the Listing Builder without leaving the platform.

Jungle Scout: Product Database + Opportunity Finder

Jungle Scout splits its product research across two complementary tools. The Product Database works similarly to Black Box with filters for demand, competition, revenue, and category. Beginners who have no idea where to start can use preset filters to discover profitable categories immediately.

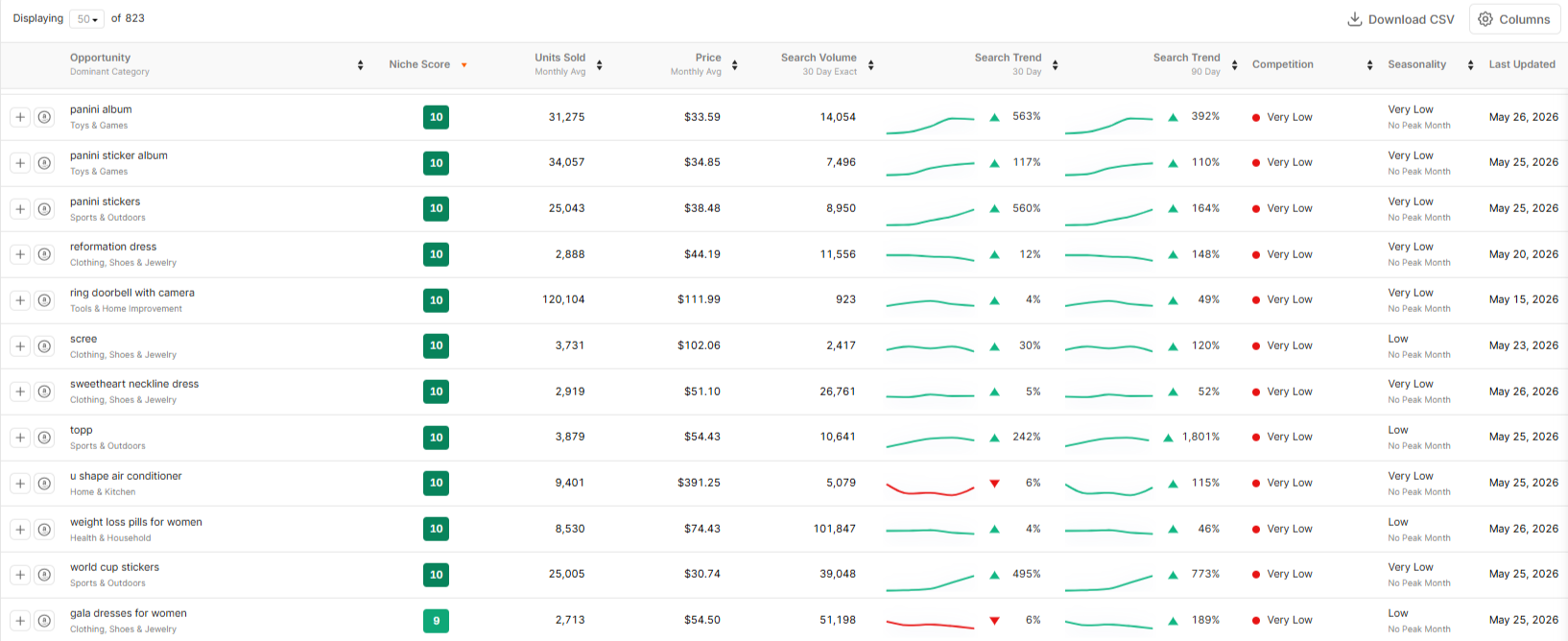

The Opportunity Finder adds something Black Box does not offer: a dedicated niche scoring system. The tool assigns a Niche Score from 1 to 10 based on demand, competition, and listing quality within a subcategory. Sellers targeting low-competition, high-demand products should aim for scores between 7 and 10.

Our Verdict: Jungle Scout wins for beginners and niche discovery thanks to the Opportunity Finder and its scoring system. Helium 10 wins for experienced sellers who want maximum filter control and tight integration with keyword tools.

Going deeper: Both tools approach product research from the bottom up, starting with individual products. SmartScout's Subcategories tool takes the opposite approach: start with 40,000+ subcategories, view revenue data and brand distribution, and then drill into individual products. This top-down method helps sellers discover profitable niches that product-level filters would never surface. See how it works in our resource guide.

Also Read: For a three-way comparison including market intelligence capabilities, check out our detailed SmartScout vs Helium 10 vs Jungle Scout breakdown.

2. Keyword Research

Helium 10: Cerebro and Magnet

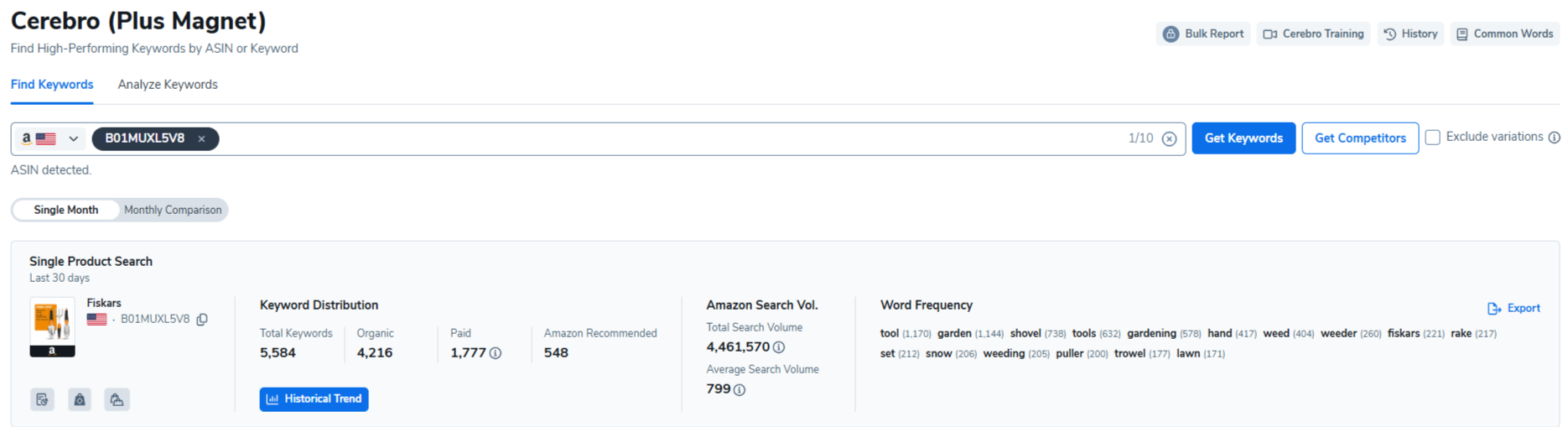

Cerebro is the most advanced Amazon keyword research tool on the market. Enter a competitor's ASIN, and Cerebro returns a complete keyword profile with search volume, organic and sponsored rank positions, the proprietary IQ Score, word frequency analysis, and top 10 title density. The IQ Score is particularly useful: a high score means strong search volume with low competition.

Magnet complements Cerebro by expanding seed keywords into comprehensive lists with monthly search volume data, trending direction, and related keyword suggestions. Both tools update their data daily.

Jungle Scout: Keyword Scout

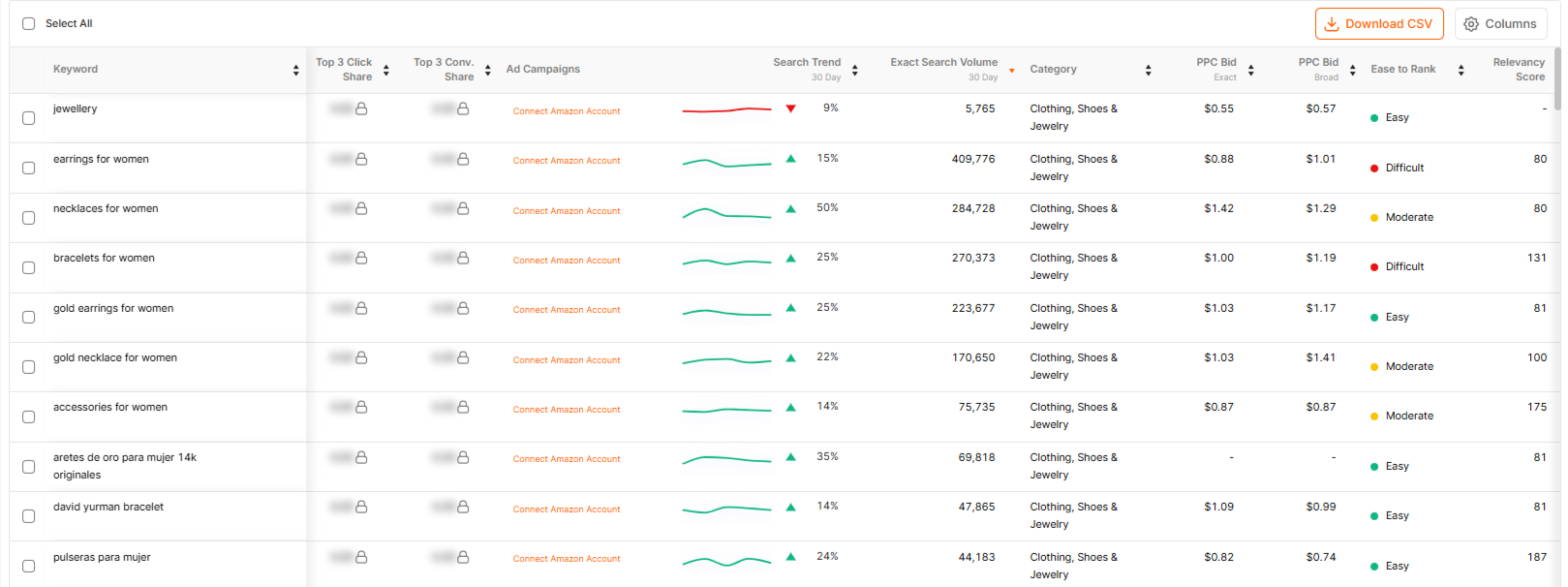

Keyword Scout provides keyword research through seed keywords or ASIN-based reverse lookup (up to 10 ASINs). You get estimated monthly searches, trend direction (up, down, or flat), competition level, and an Opportunity Score that combines volume and competition into a single metric.

Keyword Scout also shows top advertisers bidding on each keyword and provides PPC cost estimates. For sellers running or planning sponsored campaigns, this advertising context is immediately actionable. The trade-off is that Keyword Scout does not offer the same depth of filtering or the granular distribution data that Cerebro provides.

Our Verdict: Helium 10 wins. Cerebro and Magnet together represent the gold standard for Amazon keyword research. The IQ Score, daily data updates, and advanced filtering options give experienced sellers tools that Keyword Scout cannot match in raw depth. That said, Keyword Scout's simpler approach with the built-in Opportunity Score works perfectly for sellers who want actionable data without a steep learning curve.

Complementary approach: SmartScout's Keyword Detective and Search Terms Relevancy tools answer a different question than Cerebro or Keyword Scout. Instead of just showing search volume, they map the relevancy and intent behind search terms at the product and category level. Sellers who want to understand why customers search for certain products, not just how often, find this layer of context invaluable for PPC targeting and listing strategy.

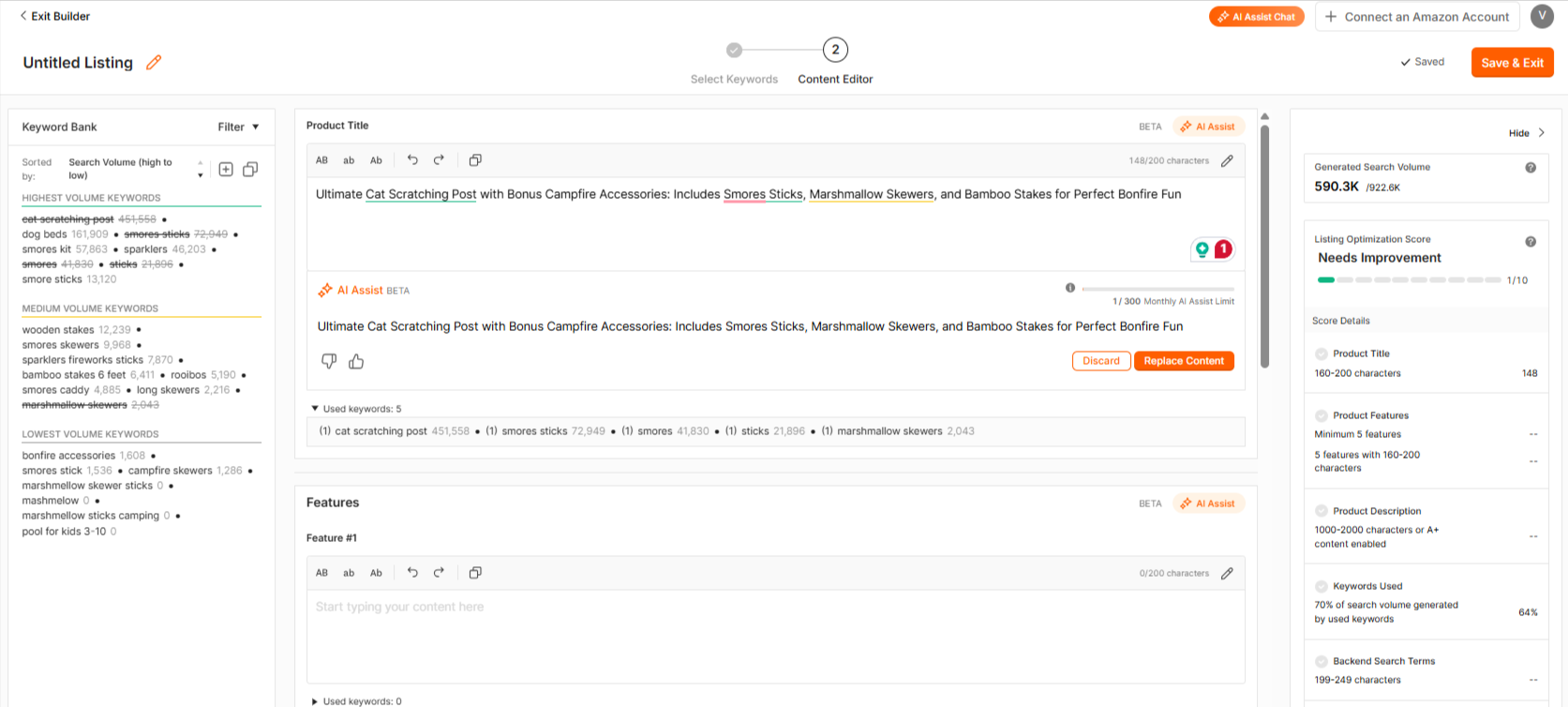

3. Listing Optimization

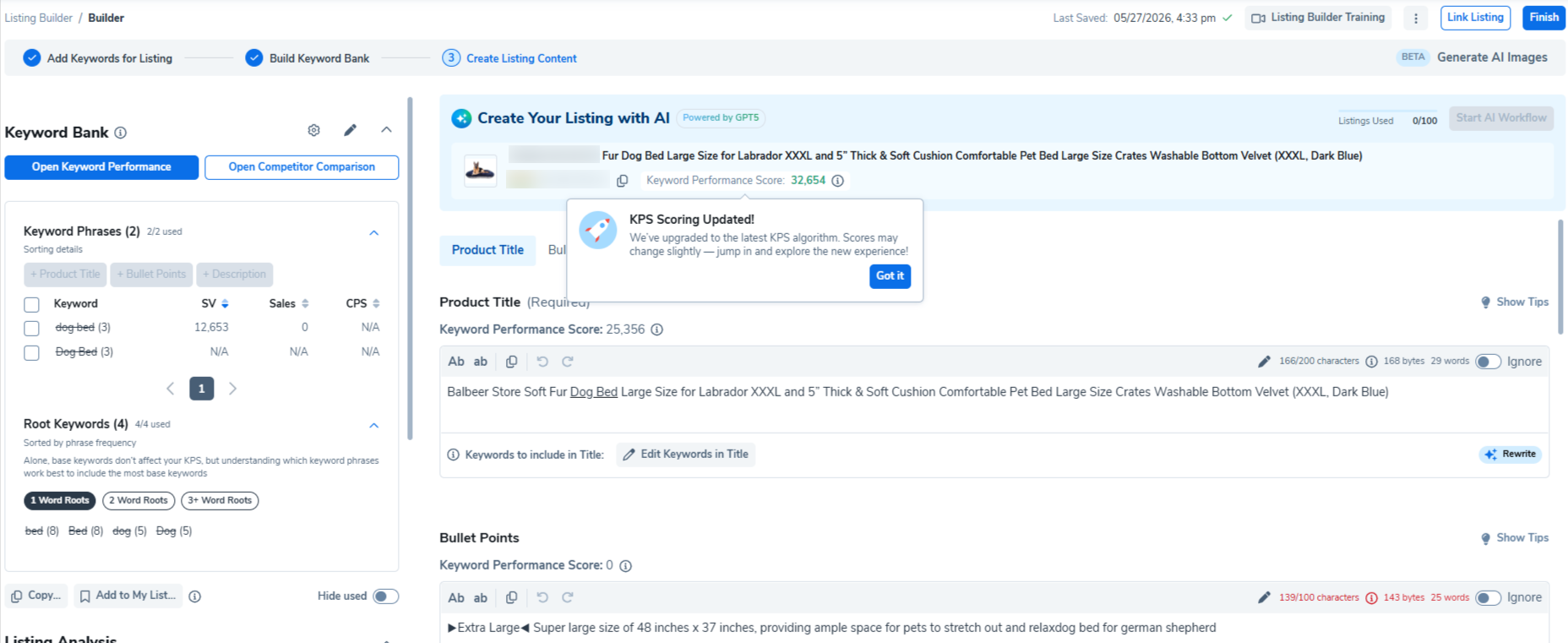

Helium 10: Scribbles and Listing Builder

Helium 10 approaches listing optimization as a two-step process. Scribbles analyzes keyword distribution across your listing components, showing where important keywords are missing from your title, bullets, description, and backend search terms. The Listing Builder then uses ChatGPT integration to generate optimized copy for each section.

For existing listings, Helium 10 provides green and red health indicators highlighting sections that need attention. The combination is powerful for sellers who already have products live and want to improve their organic rankings.

Jungle Scout: Listing Builder with AI Assist

Jungle Scout's Listing Builder pulls keywords from Keyword Scout and uses AI Assist to generate titles, bullet points, descriptions, and backend terms. The AI has improved significantly through 2025 and into 2026, now offering customer sentiment analysis and copy improvement suggestions.

One advantage Jungle Scout holds here is that AI Assist works for creating listings from scratch. You do not need an existing listing to optimize. For new product launches, you can go from keyword research to a fully drafted listing in minutes. Helium 10's Scribbles, by contrast, focuses primarily on optimizing existing listings.

Our Verdict: Tie. Helium 10 has the edge for optimizing existing listings with its detailed keyword distribution analysis and health scoring. Jungle Scout has the edge for creating new listings from scratch with AI Assist. Both platforms get the job done.

Related: SmartScout'sAI Listing Architect creates listings that combine keyword data with competitive positioning insights from SmartScout's brand and subcategory intelligence, giving your copy a strategic angle that standalone listing builders miss.

4. PPC Management

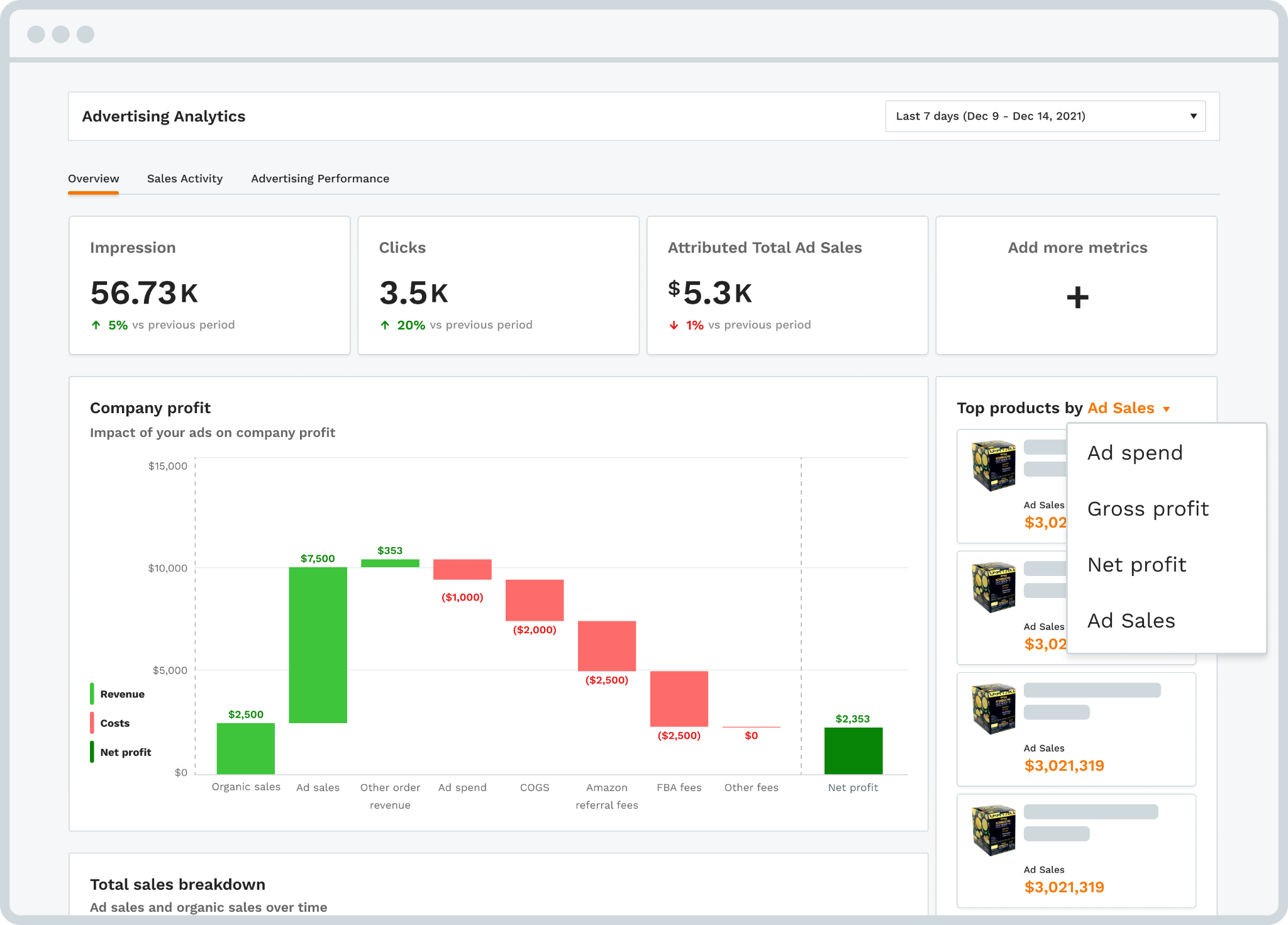

Helium 10: Adtomic (Helium 10 Ads)

Adtomic is a full-featured PPC management platform with AI-driven bid optimization, campaign structuring, budget guardrails, dayparting, and performance tracking. It integrates with Cerebro's keyword data to align targeting with search demand.

There is a catch, though. Adtomic is only fully included with the Diamond plan ($359/month). Platinum users can access basic ad features but not the full automation suite. On top of the subscription, Helium 10 charges a 2% management fee on all PPC spend managed through the platform. For sellers spending $10,000 per month on ads, that is an extra $200 in fees.

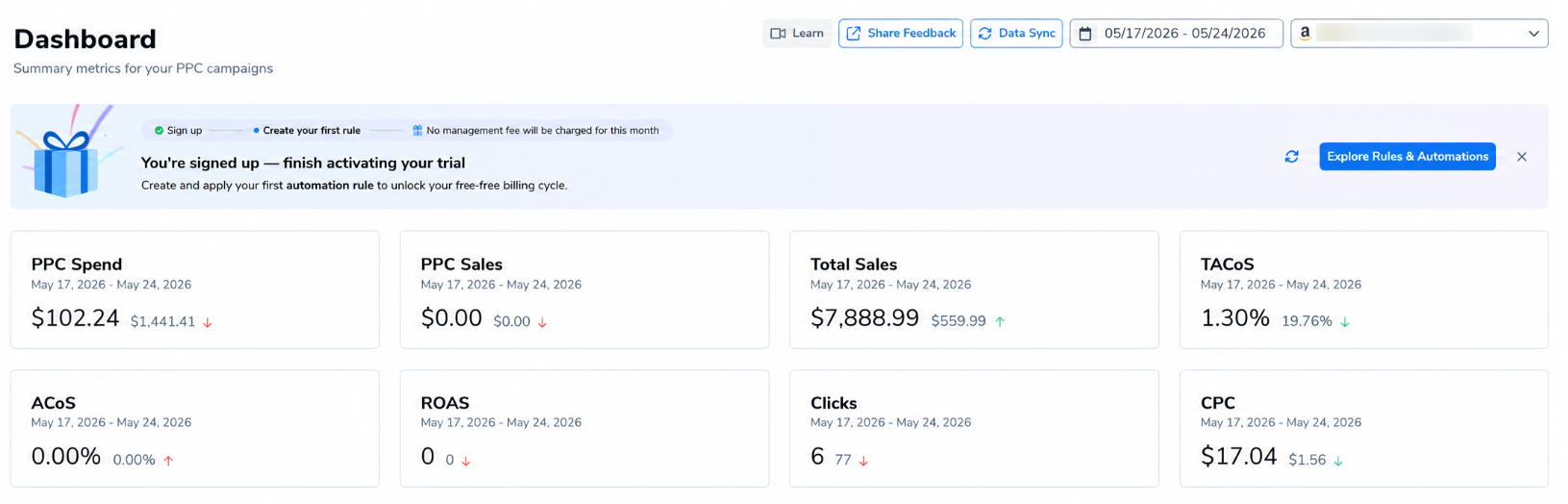

Jungle Scout: Advertising Analytics

Jungle Scout offers Advertising Analytics on Growth Accelerator plans and above. It provides campaign performance tracking, keyword-level ad data, and spending breakdowns. For enterprise brands, Jungle Scout Cobalt's Ad Accelerator adds rule-based bid automation, dayparting, and multi-account management.

The standard Catalyst plans focus on analytics and reporting rather than automated campaign management. If you want hands-off PPC optimization comparable to Adtomic, you need Cobalt's enterprise pricing.

Our Verdict: Helium 10 wins for PPC automation. Adtomic is the more mature and feature-complete PPC tool, and it is available at the Diamond tier without needing a custom enterprise quote. Jungle Scout's advertising analytics are useful for monitoring, but serious PPC management requires either manual work or upgrading to Cobalt.

PPC intelligence gap: Neither Adtomic nor Jungle Scout's Advertising Analytics shows you what your competitors are actually doing with their ad spend. SmartScout's Ad Spy fills that gap by revealing competitor keyword bidding patterns, estimated ad spend, and campaign structures. Understanding the competitive ad landscape before you set up campaigns makes every dollar you spend on Adtomic or any PPC tool more effective. Learn how to build a repeatable competitor analysis workflow.

5. Supplier Sourcing

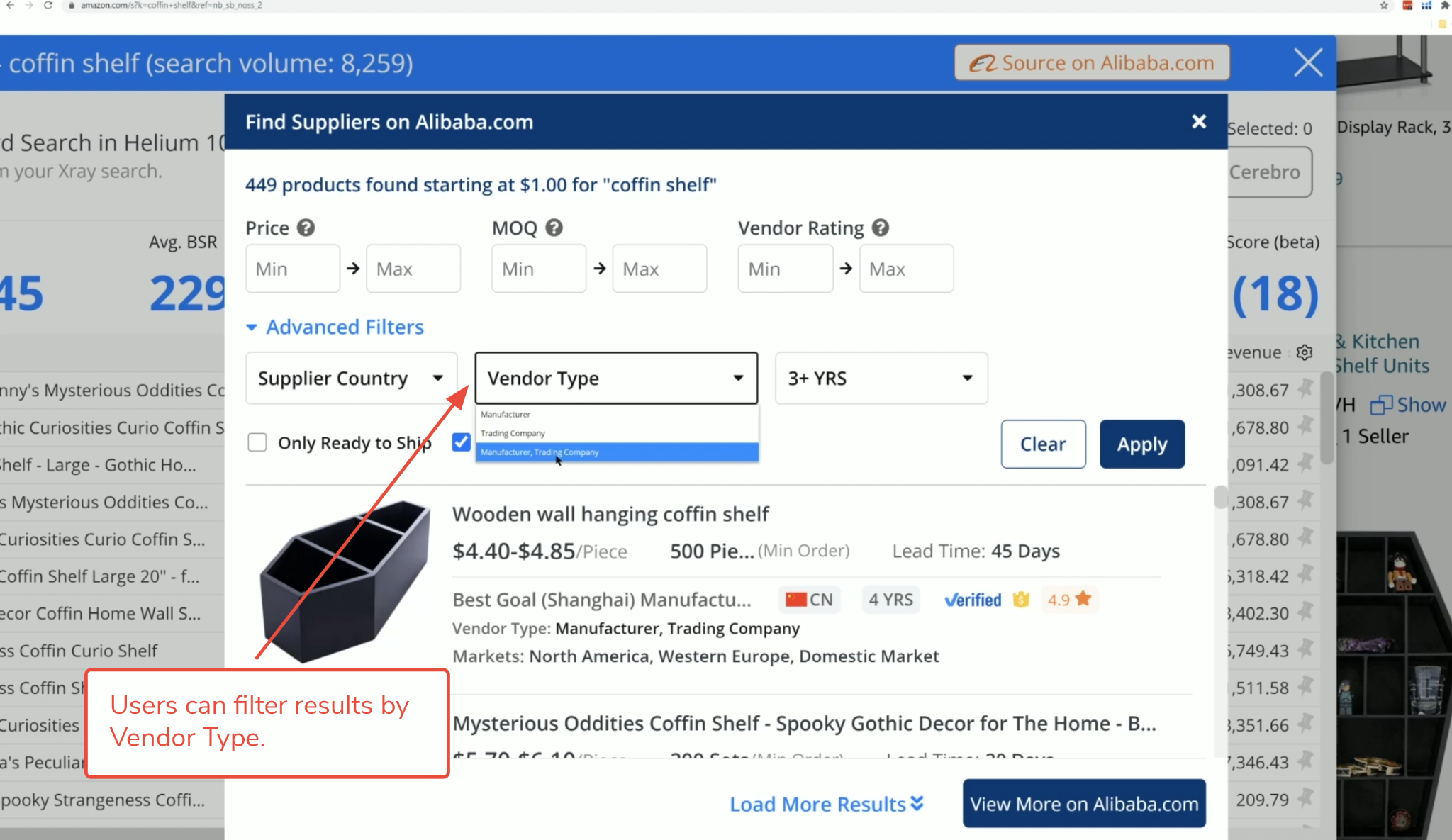

Helium 10: Supplier Finder

Helium 10's Supplier Finder is a Chrome extension feature that shows supplier information when you browse Alibaba.

You can filter by price, minimum order quantity, and ratings. It is convenient for quick lookups, but it only covers Alibaba. There is no global supplier database, no shipment history data, and no way to vet suppliers within the Helium 10 platform itself.

Jungle Scout: Supplier Database

The Supplier Database is one of Jungle Scout's standout features. It gives you access to import records for a reported 98% of Amazon sellers. You can search by product, brand, or supplier name and see exactly which manufacturers are supplying which products, along with shipment volumes, pricing, and the identity of top US customers.

This level of sourcing intelligence is invaluable for sellers who want to verify a supplier's legitimacy before placing orders. No other mainstream Amazon tool provides this depth of supplier intelligence within its standard plans.

Our Verdict: Jungle Scout wins convincingly. The Supplier Database is a genuine competitive advantage that goes far beyond Helium 10's Alibaba-only extension. For any seller who sources products from manufacturers, this single feature can justify the Jungle Scout subscription.

6. Brand and Market Intelligence

This is where both Helium 10 and Jungle Scout share a significant blind spot.

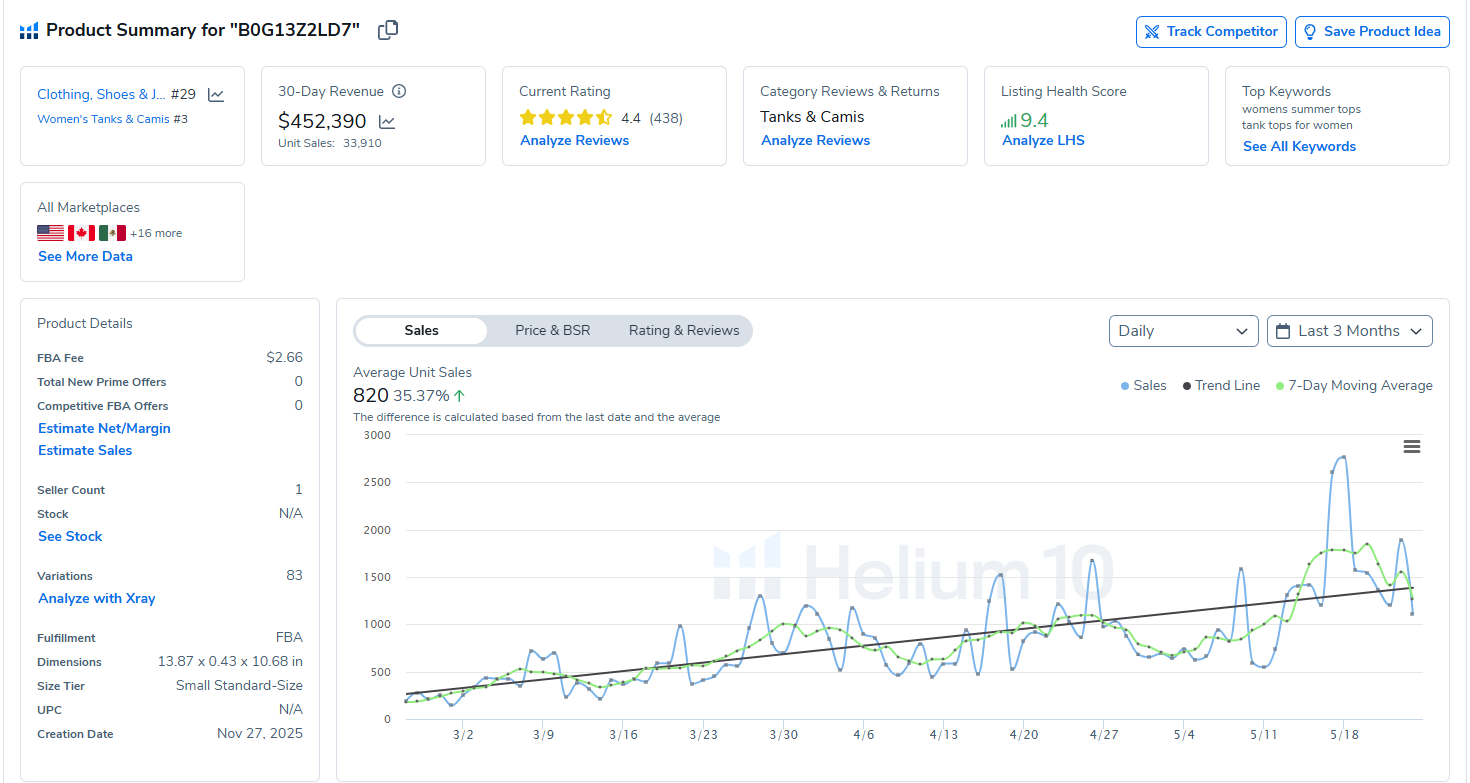

Helium 10's Market Tracker monitors competitor ASINs and tracks market share changes at the product level.

It is useful for keeping an eye on specific competitors, but it does not provide brand-wide revenue estimates, seller dynamics, or category-level competitive intelligence.

Jungle Scout's Brand Owner + CI plan ($149/month) includes competitive benchmarking and market share analysis.

Cobalt takes this further with enterprise-level intelligence. But even at these higher tiers, neither tool maps entire brand ecosystems, provides a proprietary brand health score, or visualizes how customer traffic flows between related products.

For wholesale buyers deciding which brands to approach, online arbitrage sellers evaluating seller density, or agencies pitching potential clients, product-level data alone is not enough. You need to understand brand-level dynamics: revenue distribution, seller count trends, Amazon's own in-stock rate, and competitive positioning across subcategories.

This is SmartScout's core strength. The Brand Database lets you filter through 1.5 million+ Amazon brands using 30+ parameters. The Traffic Graph visualizes how customer traffic flows between products. The Seller Map shows you exactly where Amazon sellers are located, what they sell, and how much revenue they generate. No other Amazon tool, including Helium 10 and Jungle Scout, provides this level of market intelligence. Explore the full Amazon software comparison to see where each tool fits.

7. Review Automation

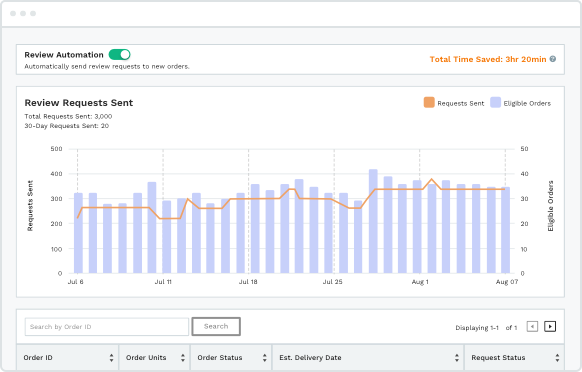

Jungle Scout includes automated review request functionality on Growth Accelerator plans and above. You can set up automated requests that follow Amazon's Terms of Service, helping you build social proof faster without manual effort.

Helium 10 does not have a built-in review automation tool. Sellers using Helium 10 need to request reviews manually through Seller Central or use a third-party service, which adds cost and complexity.

Our Verdict: Jungle Scout wins. Review automation is a core operational feature for Amazon sellers, and having it built into the platform saves both time and money. The absence of this feature in Helium 10 is a notable gap.

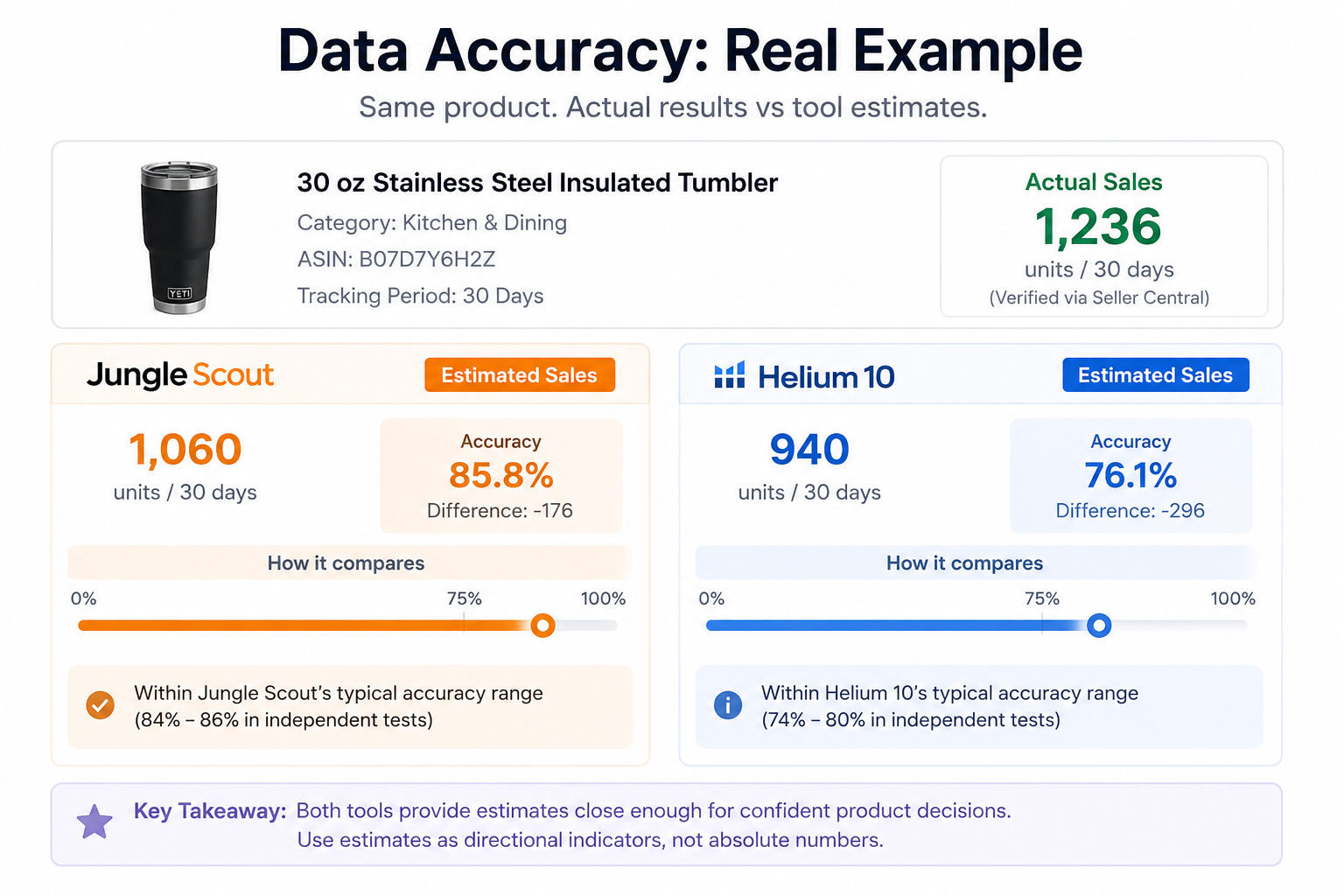

8. Data Accuracy

Accuracy is the most debated topic in every Helium 10 vs Jungle Scout comparison, and both platforms claim to be the most accurate. Here is what the independent testing actually shows.

Jungle Scout's own study claims 84% accuracy in sales estimation, placing itself first among all Amazon tools. Independent reviewers have largely confirmed this range, with most tests landing between 84% and 86%. Jungle Scout's 11 years of historical data and variation-level tracking contribute to consistently reliable estimates.

Helium 10's accuracy is more contested. Helium 10's own research claims 93.5% accuracy for normalized keyword search volume. Independent testers report sales estimation accuracy between 74% and 80%, depending on the product category and testing methodology.

The reality is that both tools provide estimates sufficient for product validation and business decisions. Neither is perfectly accurate, and treating any tool's estimates as gospel is a mistake. The smarter approach is to use estimates as directional indicators and validate with real sales data.

Our Verdict: Jungle Scout has a slight edge in overall sales estimation accuracy based on the weight of independent testing. Helium 10 has an edge in keyword search volume precision. In practice, both are reliable enough that accuracy alone should not be your deciding factor.

Related: SmartScout publishes transparent accuracy data. See how their estimates compare in the SmartScout Accuracy report.

9. Chrome Extension

Jungle Scout's Chrome Extension is available as a free standalone tool with limited functionality and as a full version included with all Catalyst plans.

It works on both Chrome and Firefox browsers. The extension provides sales estimates, BSR data, revenue figures, and basic competitive metrics directly on Amazon product pages.

Helium 10's Xray Chrome Extension is included with paid plans and provides more data points per product: estimated net profit, inventory stock levels, exact star rating breakdowns, and supplier lookup. However, it only works on Chrome.

Our Verdict: Tie with different strengths. Jungle Scout wins on browser compatibility (Chrome + Firefox) and free access. Helium 10 wins on data density per product page.

Worth noting: SmartScout also offers a free Chrome extension with 1,000 uses per month. It includes an FBA calculator with 2026 fee rates, BSR tracking, seller analytics, and a product opportunity score. No subscription required.

10. AI Tools

Both platforms invested heavily in AI features throughout 2025 and into 2026.

Helium 10 integrates ChatGPT into its Listing Builder and offers an AI-powered chat assistant within the dashboard. The AI also powers parts of Adtomic's bid optimization engine.

Jungle Scout's AI Assist covers four areas: sales analytics (automated performance insights), review analysis (customer sentiment extraction), listing building (SEO-optimized copy generation), and an always-on Q&A chat.

The integration is tighter across the platform, with AI recommendations surfacing naturally within each tool's workflow.

Our Verdict: Jungle Scout has a slight edge. AI Assist is more deeply integrated across the platform and covers more functional areas (especially review sentiment analysis and sales analytics). Helium 10's ChatGPT-powered listing builder is strong, but its AI features feel more bolted-on than natively integrated.

11. Customer Support and Training

Customer support quality has become a real differentiator between these two platforms in 2026.

Jungle Scout holds a 4.2 rating on Trustpilot with over 3,900 reviews. Users consistently praise the responsive live chat, helpful email support, and the quality of the Jungle Scout Academy training modules. The company responds to 92% of negative reviews within a week.

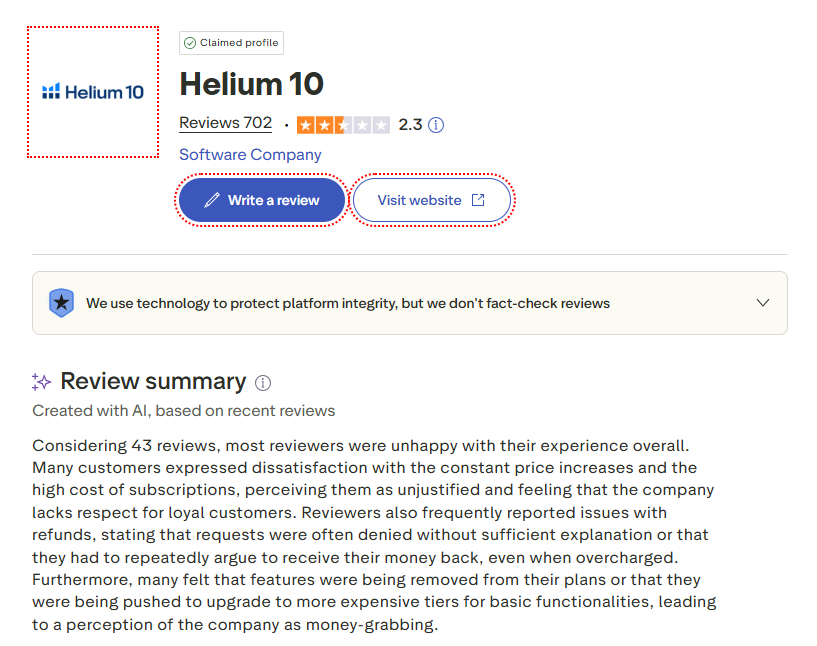

Helium 10's Trustpilot ratings are around 2.3, with the most recent scores trending lower. Common complaints include difficulty canceling subscriptions, being charged after cancellation, and slow support response times.

The Selling Guys, a well-known Amazon seller review site, reduced their Helium 10 rating from 4.8 to 4.3 in early 2026 specifically due to customer service issues and price increases. The Freedom Ticket course by Kevin King remains excellent, but it does not offset the operational support issues.

Our Verdict: Jungle Scout wins clearly. The gap in user satisfaction scores is too large to ignore. Helium 10's Freedom Ticket is a valuable training resource, but customer support quality matters when you are paying $129 to $359 per month and encounter issues.

Pricing changed significantly for both tools in 2026. Here is what you actually pay today.

Helium 10 Plans

Plan

Monthly

Annual (per month)

Platinum

$129/mo

$99/mo

Diamond

$359/mo

$279/mo

Enterprise

Custom

Custom

Helium 10 also offers a free plan with heavily restricted access. The Starter plan ($39 to $49/month) was retired in early 2026 for new users. Adtomic's full PPC automation requires the Diamond plan. A 2% ad management fee applies on top of the subscription for PPC spend managed through the platform.

Jungle Scout Catalyst Plans

Plan

Monthly

Annual (per month)

Starter

$49/mo

$29/mo

Growth Accelerator

$79/mo

$49/mo

Brand Owner + CI

$149/mo

$129/mo

Cobalt (Enterprise)

Custom

Custom

All Catalyst plans include a 7-day money-back guarantee. The Growth Accelerator plan is widely considered the best value, unlocking the Supplier Database, Review Automation, Inventory Manager, and Advertising Analytics at $79/month (or $49/month billed annually).

Our Verdict: Jungle Scout is significantly more affordable at every tier. Jungle Scout's Growth Accelerator at $49/month (annual) includes features that Helium 10 locks behind the $279/month Diamond plan. Even Jungle Scout's top-tier Brand Owner + CI plan ($129/month annual) costs less than Helium 10's entry-level Platinum at $129/month.

Budget tip: SmartScout's Basic plan starts at $29/month, and the Essentials plan ($97/month) includes brand analytics, Seller Map, and Traffic Graph. A seller running SmartScout Essentials ($75/month annual) and Jungle Scout Growth Accelerator ($49/month annual) pays just $124/month total, which is less than Helium 10 Platinum alone. That combination gives you market intelligence, product research, supplier sourcing, and review automation. See SmartScout pricing for full plan details.

By this point, the pattern should be clear: neither platform is objectively better than the other. Helium 10 offers greater depth, automation, and marketplace coverage, while Jungle Scout prioritizes simplicity, affordability, and product discovery. Here's a quick look at where each platform shines and where it falls short.

Pros and Cons of Helium 10

Pros

Industry-leading keyword research with Cerebro and Magnet

Advanced PPC automation through Adtomic

Supports Amazon, Walmart, and TikTok Shop

Extensive suite of tools for scaling businesses

Includes Freedom Ticket training for paid users

Cons

Significantly more expensive than Jungle Scout

Steeper learning curve due to the large number of tools

Some advanced features require higher-tier plans

Customer support receives mixed reviews from users

Limited supplier intelligence compared to Jungle Scout

Pros and Cons of Jungle Scout

Pros

Beginner-friendly interface and workflows

Strong product research and validation tools

Best-in-class Supplier Database

Built-in review automation and inventory management

More affordable pricing across all tiers

Cons

Less advanced keyword research than Helium 10

PPC tools focus more on analytics than automation

Amazon-focused with no Walmart or TikTok Shop support

Fewer advanced optimization features for large sellers

Limited competitive intelligence compared to specialized Amazon research platforms

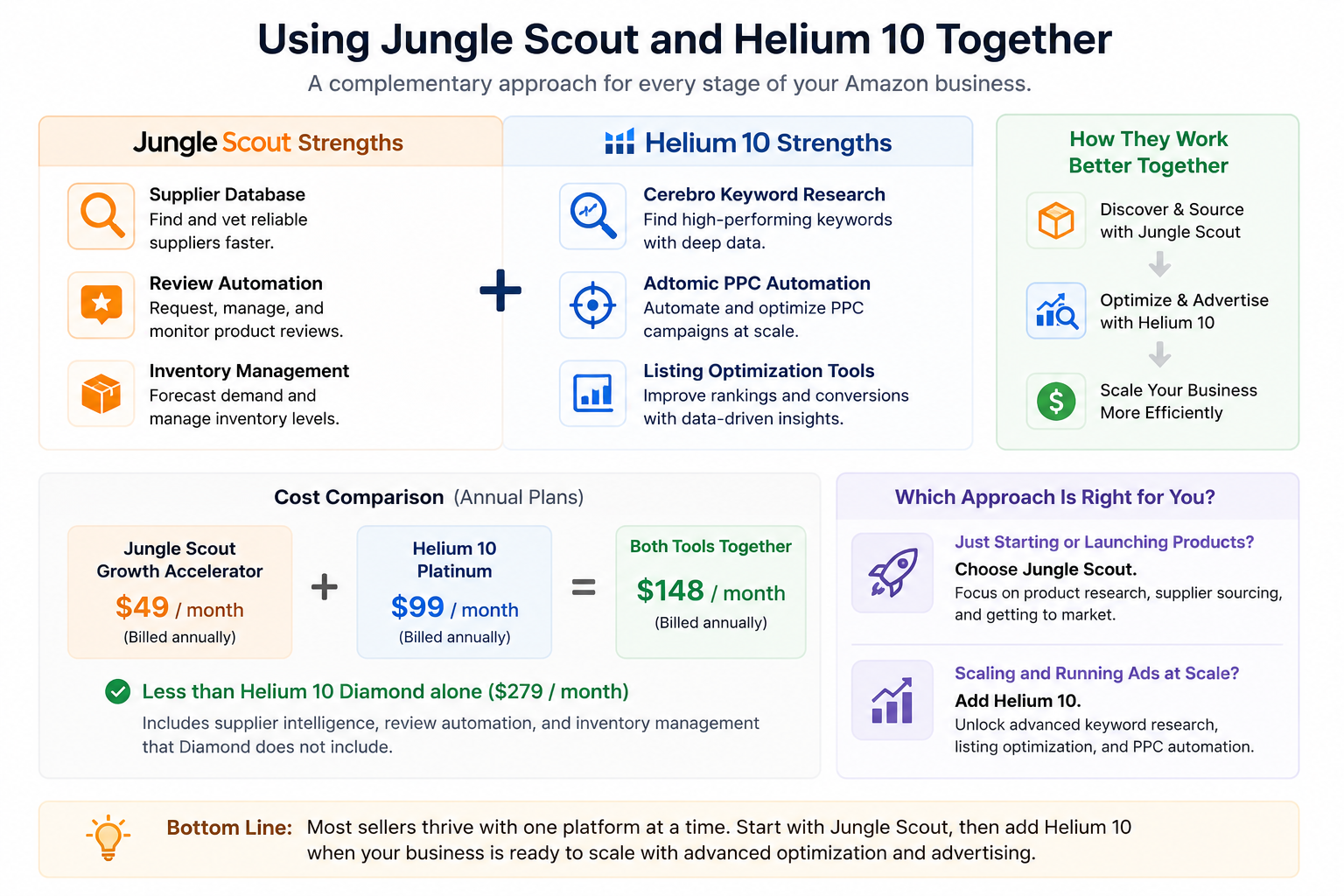

Can You Use Helium 10 and Jungle Scout Together?

Some sellers run both tools simultaneously, and it is not as redundant as it sounds.

The strongest case for using both is pairing Jungle Scout's Supplier Database and Review Automation with Helium 10's Cerebro keyword research and Adtomic PPC automation. Jungle Scout handles the product discovery and sourcing phase, while Helium 10 handles the optimization and advertising phase.

The combined cost of Jungle Scout Growth Accelerator ($49/month annual) and Helium 10 Platinum ($99/month annual) comes to $148/month. That is still less than Helium 10 Diamond alone ($279/month annual), and you get supplier intelligence, review automation, and inventory management that Diamond does not include.

For most sellers, though, choosing one platform is the pragmatic move. Pick Jungle Scout if you are still in the product research and launch phase. Add Helium 10 when your business demands advanced keyword optimization and PPC automation at scale.

The Complete Amazon Seller Stack: Filling the Gaps

Helium 10 and Jungle Scout both excel at product-level operations (keyword research, listing optimization, PPC management, supplier sourcing), but neither provides the market intelligence layer that separates good product decisions from great ones.

Here’s what most sellers do:

Market intelligence (brand analytics, subcategory revenue, seller mapping, traffic flow) for deciding WHERE to compete

Product research and validation (product databases, keyword research, demand estimation) for deciding WHAT to sell

Operational optimization (listing SEO, PPC automation, review management, inventory tracking) for deciding HOW to sell better

Helium 10 and Jungle Scout both cover the second and third layers exceptionally well. They also offer limited market-level visibility through tools such as Market Tracker and Jungle Scout's Market Intelligence capabilities.

The distinction is that these features are primarily designed to monitor products and competitors you already know about. They are less focused on exploring entire categories, evaluating brand ecosystems, mapping seller networks, or identifying market opportunities before product research begins.

However, Helium 10’s market intelligence tool comes as an add-on, whereas Jungle Scout’s unlocks when you go for the highest-tier plan.

SmartScout fills the market intelligence gap at a lower cost. The Subcategories tool maps 40,000+ niches with revenue data. The Brand Database filters 1.5M+ brands by 30+ parameters. The Traffic Graph reveals product relationships and ad targeting opportunities. The Seller Map shows geographic seller distribution worldwide. And the Ad Spy exposes competitor advertising strategies. None of these capabilities exist in Helium 10 or Jungle Scout at any price tier. Book a free SmartScout demo to see how it complements your existing toolkit.

Conclusion: Jungle Scout for Getting Started, Helium 10 for Scaling Up

After testing both platforms extensively, the pattern is clear: these tools serve different stages of the Amazon selling journey.

Jungle Scout Catalyst is the stronger choice for sellers who are finding products, validating demand, sourcing suppliers, launching listings, and building review momentum. The Opportunity Finder, Supplier Database, and Review Automation create a cohesive workflow that takes you from idea to live product with minimal friction. The pricing is fair, the interface is clean, and the customer support is consistently excellent.

Helium 10 is the stronger choice for sellers who have established products and want to maximize their performance. Cerebro's keyword depth, Adtomic's PPC automation, and the multi-marketplace support (Amazon + Walmart + TikTok Shop) give scaling sellers tools that Jungle Scout does not match. The pricing is steep, the learning curve is real, and the support could be better, but the raw capability is undeniable.

If budget forces a single choice: pick Jungle Scout if you are a beginner want to scale on Amazon, and consider Helium 10 when you are a high-end seller and need deeper optimization firepower.

SmartScout offers the capability of both Helium 10 and Jungle Scout at a fraction of the cost. Additionally, you get exceptional features like AI Listing Architect, Traffic Graph, Seller Map, and access to 40K categories, at a starting price of $29/month. New users can start with a risk-free 7-day money-back guarantee.

TikTok Shop crossed $64.3 billion in global GMV in 2025. Social commerce in the US alone is on pace to surpass $100 billion by the end of this year. These are not speculative projections. This is where buyer attention is moving, and the sellers who are winning on TikTok Shop right now share one thing in common: they stopped guessing before everybody else did.

TikTok's commerce engine moves fast enough to break manual research. A product can go from zero to 50,000 units in a week off one viral video, and by the time you spot it, the market is saturated, and margins have collapsed. Views and follower counts say nothing about actual purchases, and Seller Center only shows your own store. You get no read on what competitors are doing or which categories are heating up.

That blind spot is what we built SmartScout TikTok Shop Analytics to close. It brings the category-first approach behind our Amazon Subcategories and Brand Database tools to TikTok Shop, mapping the market before you commit to a product.

To set the context, we tested the top platforms in this space across product research, category intelligence, competitor analysis, creator attribution, and ad tracking, and ranked them on the depth of actionable data they actually deliver.

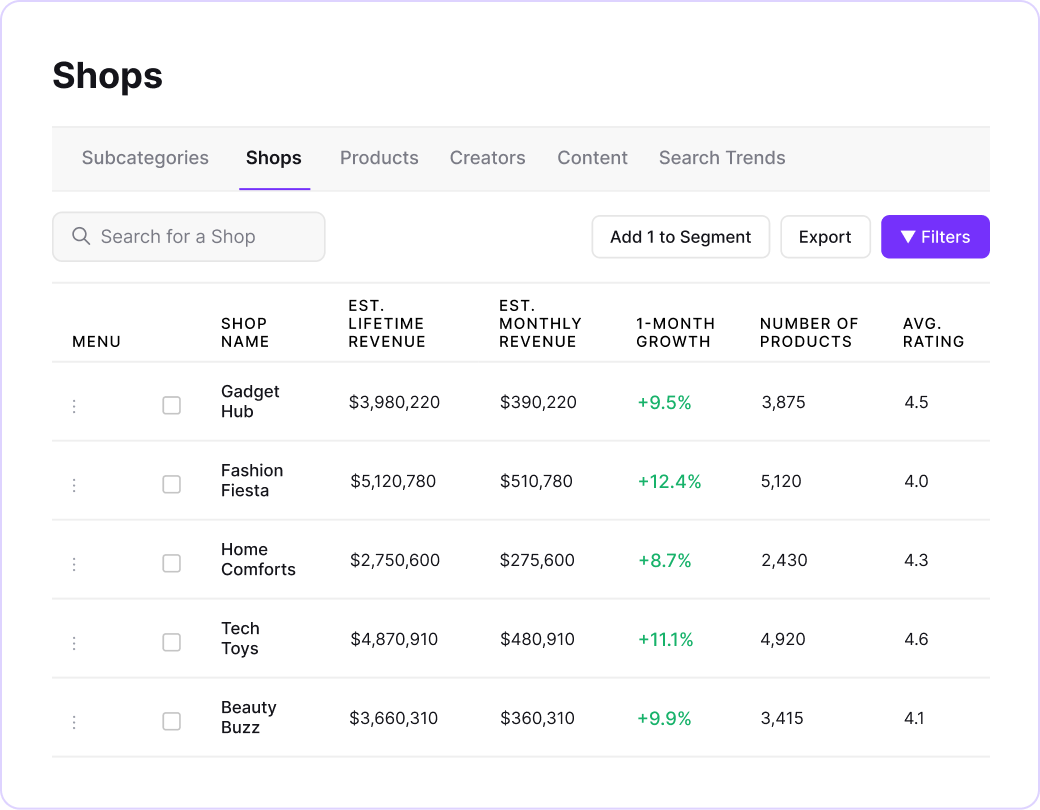

9 Best TikTok Shop Analytics Tools for Product & Category Research

Here is how the nine platforms stack up at a glance, from category-level market intelligence down to single-purpose ad and own-shop tools, before we break each one down in detail below.

Tool

Key Data Points

Strongest For

Free Trial

Starting Price

SmartScout

Category, shop, product, creator, trend

Category-level market intelligence

Coming soon

$29/mo

Kalodata

Product, creator, video, shop, livestream

Product discovery + creator attribution

Yes (7 days)

$49.99/mo

FastMoss

Product, shop, ad, live, creator

Enterprise monitoring + live commerce

Yes (7 days)

$29/mo

Helium 10

Listing converter, profitability, influencer

Amazon-to-TikTok expansion

Free plan (limited)

$129/mo

EchoTik

Product, creator, shop, live (Chrome ext.)

Free research for beginners

Free plan

$13.9/mo

Shoplus

Product, trend, creator, shop

Budget product research

Free tier

$49/mo

PiPiADS

Ad creatives, product discovery via ads

TikTok ad creative intelligence

Trial available

$49/mo

Tabcut

Product, shop, category, API

API access for custom reporting

Free plan

$59/mo

TikTok Seller Center

Own shop: orders, revenue, fulfillment

Your own store analytics

Free

Free

Not sure which of these fits your stage and budget? Answer a few quick questions below, and we'll point you to the tool (or stack) that matches how you actually run your TikTok Shop business, from first product test to full agency monitoring.

Implement the tool (check tab 2 for the tool’s HTML code)

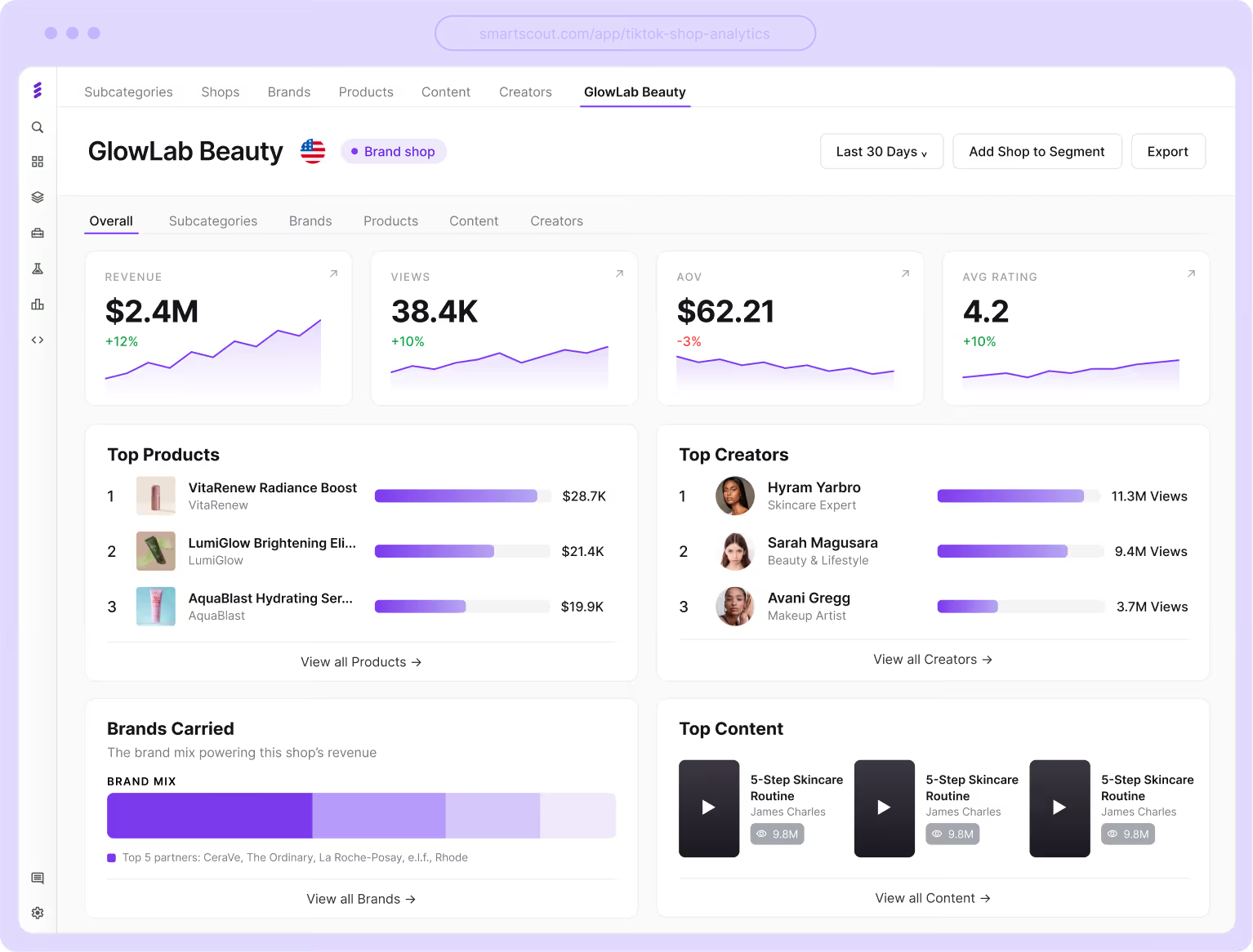

1. SmartScout: Best for TikTok Shop Category Analysis and Market Intelligence

Parameter

Details

Tool name

SmartScout TikTok Shop Analytics

Standout feature

White-space opportunity finder that identifies underserved TikTok Shop categories by revenue, competition density, and growth rate

Data source

Proprietary algorithms processing TikTok Shop category, shop, product, creator, and video data (same engine behind SmartScout's Amazon analytics)

Starting price

$29/month (existing plans). TikTok-specific pricing at launch.

Free trial/plan

7-day money-back guarantee on all plans. Early access registration open.

Every other tool on this list starts the same way: type in a keyword or browse a list of trending products. That workflow answers one question: what is selling on TikTok right now? It does not tell you whether the category behind that product is growing or contracting. It does not tell you whether three shops control 80% of the revenue or whether the market is fragmented enough for a new entrant. And it definitely does not tell you whether the trend you spotted yesterday will still exist next month.

SmartScout is building something fundamentally different for TikTok Shop. Instead of starting with products, it starts with the market structure itself. If you have used SmartScout for Amazon, the philosophy is identical to what the Subcategories tool and Brand Database already do: map the landscape first, then decide where to compete.

What SmartScout TikTok Analytics will offer

The Category Analysis module is the flagship. It will provide revenue estimates for TikTok Shop categories, market share breakdowns by the top shops in each category, product concentration metrics, and a white-space opportunity finder that flags niches where demand outpaces supply. No other TikTok analytics tool currently offers this kind of category-level intelligence.

Shop Analysis goes beyond surface metrics. Instead of just showing a shop's product count and follower total, SmartScout will estimate revenue, map the product mix, track growth trajectory over time, and show creator partnership density. You will be able to evaluate whether a competitor's growth is sustainable or driven by a single viral moment.

Creator and Video Performance will connect content directly to commerce. The platform tracks which creators actually drive purchases (not just views), which video formats convert at the highest rate, and which content angles are gaining traction within specific categories. This bridges the gap between social media vanity metrics and real sales attribution.

Trend Validation is where most sellers lose money. A product trending on TikTok is not automatically a good business opportunity. SmartScout will analyze trends through sales velocity, creator activity patterns, and shop-level adoption rates rather than relying on view counts. If a product is being pushed by 200 creators but only 3 shops are actually fulfilling orders, that is a different signal than a product with 40 active shops and steady daily volume.

SmartScout pricing and availability

SmartScout's existing Amazon plans start at $29/month (Basic) and $97/month (Essentials). Pricing for TikTok Shop analytics will be announced at launch. Sellers who already use SmartScout for Amazon will get a unified research experience across both platforms, which is a significant advantage for brands and agencies operating on multiple channels.

Category-level revenue estimates with market share breakdowns by top shops, product concentration metrics, and a white-space opportunity finder that flags niches where demand outpaces supply

Shop-level competitive profiling that estimates revenue, maps product mix, tracks growth trajectory, and measures creator partnership density for any TikTok storefront

Creator and video performance tied to actual commerce: which creators drive purchases (not just views), which video formats convert, and which content angles gain category-specific traction

Trend validation engine that analyzes trends through sales velocity, creator adoption patterns, and shop-level traction rather than relying on view counts or engagement rate

Unified cross-platform intelligence for sellers and agencies operating on both Amazon and TikTok Shop from a single provider

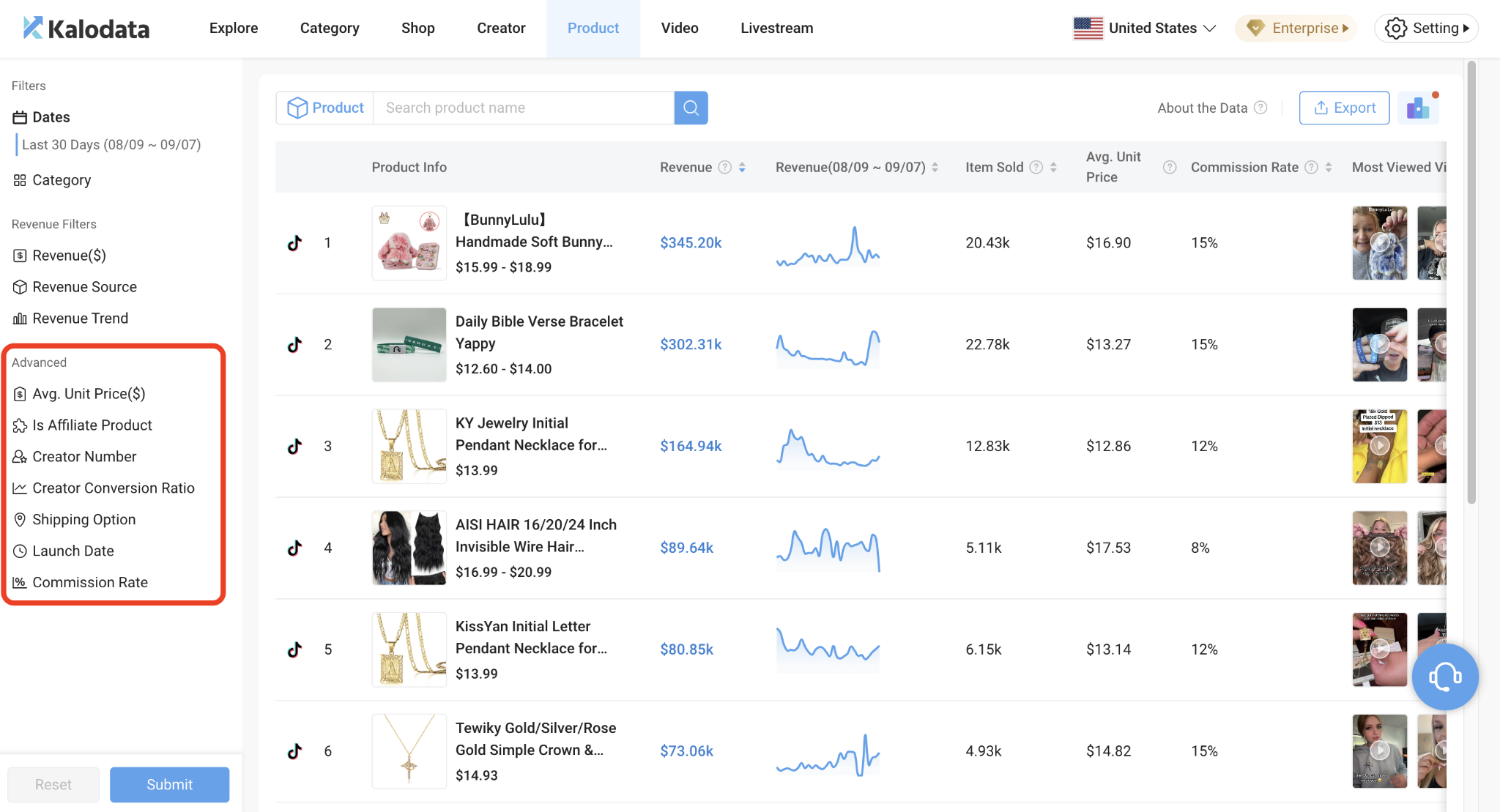

2. Kalodata: Best for TikTok Shop Product Research and Creator Discovery

Parameter

Details

Tool name

Kalodata

Standout feature

Creator-to-sales attribution that tracks how many actual units each creator moved, not just their follower count or engagement rate

Data source

Proprietary AI models trained on 100M+ TikTok Shop products, 200M+ creator profiles, and 300M+ videos. Models retrain daily.

Starting price

$45.99/month (Starter)

Free trial/plan

7-day free trial, no credit card required

The team behind Kalodata came directly from TikTok's own Global E-Commerce Division. These are the people who helped build TikTok Shop from the ground up, and that insider pedigree shows in how the platform handles data. Kalodata does not just scrape public metrics. It processes signals across its massive database to surface patterns that manual research would never catch.

Where Kalodata earns its reputation is in connecting creator activity to actual sales. Most tools show you a creator's follower count and engagement rate, which tells you almost nothing about whether partnering with them will generate orders. Kalodata tracks sales attribution at the creator level, so you can see exactly how many units a creator moved last month, what their average commission rate is, and which product categories they convert best in.

Key features

Margin estimation that factors in product price, TikTok's category-specific platform fees (2% to 8%), and affiliate commission rates before you commit to sourcing

AI-powered video analysis on Professional/Enterprise plans that identifies which content hooks, formats, and scripts are converting in any given category right now

Competitor shop revenue tracking with product-level sales breakdowns and historical performance curves

Livestream analytics covering viewer-to-buyer conversion rates, peak engagement moments, and product-level GMV per session

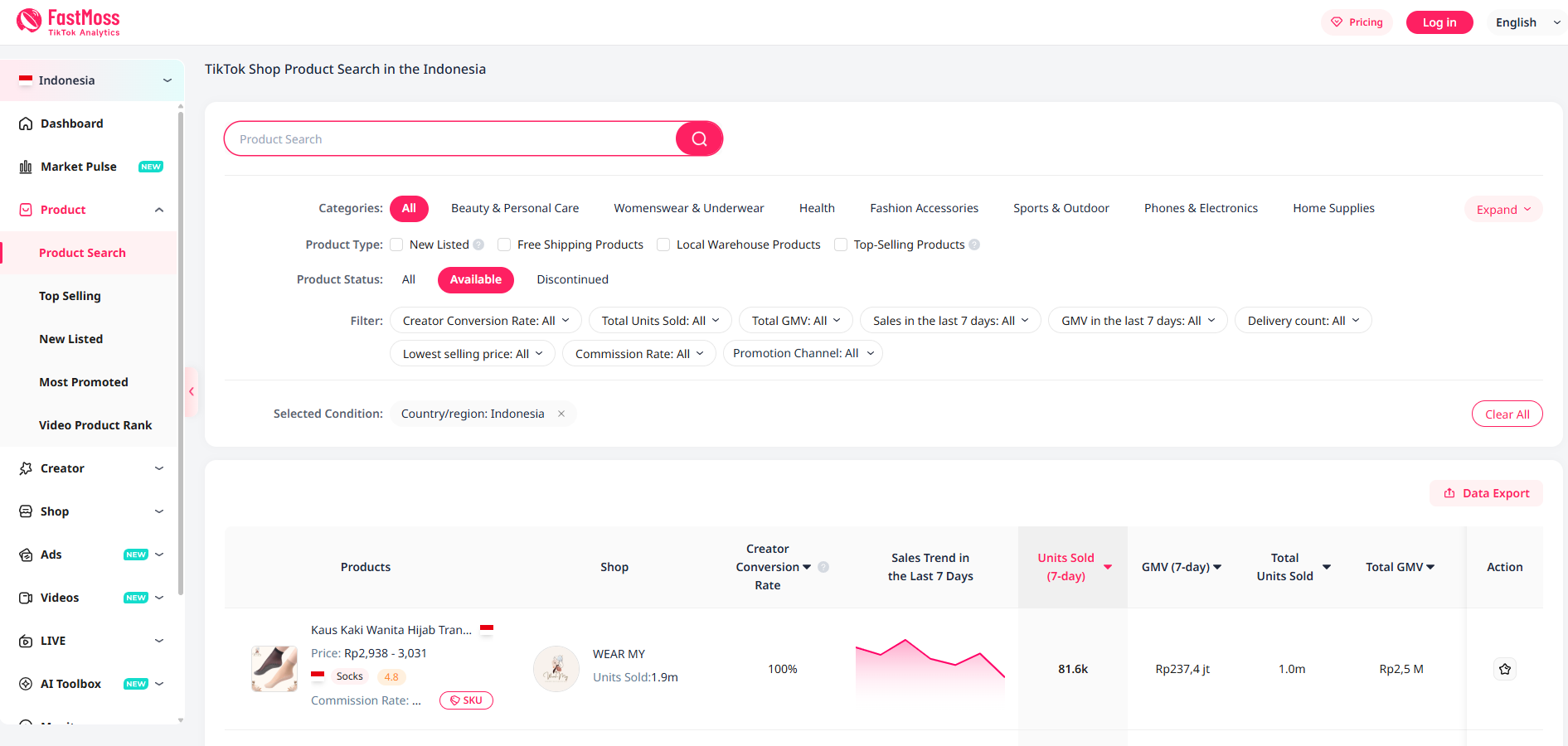

3. FastMoss: Best TikTok Shop Competitor Analysis Tool for Agencies

Parameter

Details

Tool name

FastMoss

Standout feature

Daily Shop Index Ranking that ranks top-performing TikTok Shops globally and by region, updated every 24 hours

Data source

Proprietary data collection across TikTok Shop storefronts, ad ecosystem, livestreams, and creator activity. Longest historical data windows in the category.

Starting price

$29/month (basic access)

Free trial/plan

7-day free trial (auto-renewing subscription)

Picture this: it is Monday morning, and you manage TikTok Shop operations for five client brands. You need to know which competitor launched a new product over the weekend, which creator partnership drove a revenue spike for a rival shop, and whether the category you recommended last month is still growing or starting to flatten. That is the workflow FastMoss was built for.

The platform tracks an enormous volume of TikTok Shop data with some of the longest historical windows in the category. The Shop Module is the centerpiece. You can analyze any TikTok Shop's estimated daily and monthly revenue, product mix, top-selling items, creator partnerships, and fulfillment patterns. The Shop Index Ranking updates daily and ranks the top-performing shops globally and by region, which gives agencies a quick competitive pulse without running custom reports.

Live commerce analytics separate FastMoss from lighter tools. TikTok Shop livestreaming is a massive sales channel (particularly in Southeast Asian markets), and FastMoss tracks peak viewership during live sessions, which products drove the most add-to-cart actions, average viewer duration, and per-session GMV. For brands running live shopping campaigns, this granularity means you can optimize every single session rather than guessing what worked.

Key features

Live commerce session analytics tracking peak viewership, which price points triggered add-to-cart actions, average viewer duration, and per-session GMV for brands running live shopping campaigns

Ad monitoring module that surfaces competitor ad creatives, estimated spend by category, and campaign format trends before they affect your organic rankings

Multi-region data coverage with the ability to compare shop performance across the US, UK, Southeast Asia, and other TikTok Shop markets simultaneously

Historical data windows significantly longer than competing platforms, enabling seasonal trend analysis and year-over-year performance benchmarking

4. Helium 10: Best for Expanding from Amazon to TikTok Shop

Parameter

Details

Tool name

Helium 10

Standout feature

Listing Converter that automatically reformats up to 20 Amazon parent ASINs into TikTok Shop-ready listings in minutes

Data source

Amazon Seller Central API integration for listing data. TikTok Shop Seller Center integration for performance tracking. No proprietary TikTok market data.

Starting price

$129/month (Platinum, basic TikTok access)

Free trial/plan

Free plan with heavily limited tool access. 7-day trial on Diamond plan.

Helium 10 does not belong in the same category as Kalodata or FastMoss. It is not a TikTok-native analytics platform, and it does not pretend to be. What Helium 10 does, and does well, is solve a specific operational pain point: the hours of manual work required to take an Amazon product catalog and get it onto TikTok Shop.

The Listing Converter handles the bulk of that friction. Titles get reformatted for mobile-first reading, descriptions get rewritten to match TikTok's content requirements, and image specifications get adjusted automatically. The Profitability Calculator factors in TikTok's category-specific fees so you can evaluate margins before committing. And the Profits Dashboard tracks revenue across Amazon, Walmart, and TikTok in a single unified view.

Key features

Amazon MCF integration that lets you fulfill TikTok Shop orders from your existing FBA inventory without setting up a separate logistics operation

Influencer Finder with filtered search by niche, follower range, and engagement metrics, plus bulk invitation tools for creator outreach at scale

Cross-channel profit attribution that separates TikTok ad spend, fulfillment costs, and net margins from your Amazon and Walmart operations

The limitation is significant: Helium 10 provides zero TikTok-native product research, zero category analysis, and zero competitor shop intelligence. If you want to discover what is selling on TikTok, you need a different tool entirely.

Related: See our full SmartScout vs Helium 10 comparison for a detailed breakdown of how these platforms differ.

5. EchoTik: Best Free TikTok Shop Analytics Tool for Beginners

Parameter

Details

Tool name

EchoTik

Standout feature

Chrome extension that overlays product, creator, and shop data directly on your TikTok feed while you scroll. No tab switching required.

Data source

Public TikTok Shop data processed through proprietary estimation models. Lighter data coverage than Kalodata or FastMoss.

Starting price

$13.9/month (Basic)

Free trial/plan

Free plan with real data, no credit card, no time limit

$0/month. That is what it costs to start using EchoTik, and the free plan is not a gated trial that expires in 7 days. You get real product data, creator analytics, and shop tracking with no credit card and no time limit.

The Chrome extension is the feature that makes EchoTik stand out from everything else on this list. Instead of opening a separate dashboard, you get TikTok Shop data overlaid directly on your feed as you scroll. Product estimates, creator metrics, and shop performance appear in context, right next to the content you are already watching. For sellers who do most of their research inside TikTok itself, this workflow eliminates the constant tab-switching that other tools require.

EchoTik covers the basics well (product discovery, creator profiles, shop tracking, live stream monitoring), but the data does not go as deep as Kalodata or FastMoss on any individual metric. There is no category-level market sizing, no long historical data windows, and no AI-powered trend forecasting. Think of EchoTik as the tool that tells you enough to make a first move, not the tool that gives you full conviction.

Key features

AI trend detection that flags products gaining momentum before they peak, surfacing early signals that manual browsing would miss

Browser compatibility across Chrome and Firefox, unlike most competitors, which support Chrome only

Shop-level tracking and live stream monitoring are included in the free tier, giving beginners competitive visibility without any financial commitment

6. Shoplus: Budget-Friendly TikTok Shop Product Research Tool

Parameter

Details

Tool name

Shoplus

Standout feature

Hourly data updates on paid plans for near-real-time visibility into which products are gaining traction right now

Data source

TikTok Shop public data with proprietary sales estimation algorithms. Smaller database than Kalodata or FastMoss.

Starting price

$49/month

Free trial/plan

Free tier with limited product searches and data access

Before Shoplus, the alternative was scrolling TikTok for hours, screenshotting products that looked popular, and trying to reverse-engineer sales volume from comment counts. Shoplus replaces that entire process with a structured dashboard of trending products, sales estimates, and category breakdowns. For sellers who just need a starting point for product ideas, it gets the job done at a price that does not require a second thought.

The limitations surface quickly as you scale. Historical data is capped at 90 days. There is no competitive shop tracking. And some users report inconsistent accuracy in sales estimates. Use Shoplus for idea generation, then move to a deeper tool when your TikTok Shop revenue justifies the upgrade.

Key features

Category browsing with basic revenue estimates and product concentration data, useful for initial niche exploration

Creator discovery module with filtering by niche and follower range for finding potential affiliate partners

Simple, clean interface that requires zero learning curve. Open it, filter by category, and browse trending products immediately.

7. PiPiADS: Best TikTok Shop Ad Spy Tool

Parameter

Details

Tool name

PiPiADS

Standout feature

20M+ TikTok ad creative database with filters for engagement, country, format, run time, and ROAS signals

Data source

TikTok Ads Library data processed through proprietary tracking and estimation models. Focused entirely on paid advertising.

Starting price

$49/month (Starter)

Free trial/plan

Trial available (limited)

Follow the ad spend, not the views. That is the logic behind PiPiADS. If a seller is spending money to advertise a product on TikTok, that product almost certainly has margins strong enough to support the ad cost. PiPiADS tracks over 20 million TikTok ad creatives and lets you filter by engagement, country, ad format, run duration, and conversion signals to identify the campaigns that are actually working.

PiPiADS does not cover organic product trends, shop analytics, category intelligence, or creator discovery. It is a specialist, and at $77/month for the entry tier, you are paying for one capability. For sellers who spend heavily on TikTok advertising, that single capability is worth the cost.

Key features

Reverse-engineering workflow: find products validated by sustained paid promotion (30+ day ad runs with strong ROAS), not just organic virality

Ad creative analysis showing which hooks, formats, and content angles drive the highest conversion rates in each product category

Landing page tracking that connects ad creatives to their destination shop pages, revealing the full funnel from impression to purchase

Related: For Amazon advertising intelligence, SmartScout's Ad Spy provides comparable competitor ad tracking across the Amazon marketplace.

8. Tabcut: Best for API Access to TikTok Shop Data

Parameter

Details

Tool name

Tabcut

Standout feature

API access that lets development teams pull TikTok Shop product, shop, and category data directly into custom dashboards and automated reporting pipelines

Data source

TikTok Shop public data processed through proprietary models. Category rankings and shop metrics available via both web interface and API.

Starting price

$59/month

Free trial/plan

Free plan with basic web access

Most TikTok Shop analytics tools assume you want a dashboard. Tabcut assumes you might want to build your own. The platform provides product research, shop analytics, and category-level data through a web interface that is functional if not particularly polished. But the real differentiator is the API access on higher plans, which lets development teams pull TikTok Shop data directly into internal dashboards, spreadsheets, or automated reporting pipelines.

For agencies with proprietary reporting stacks or brands with data engineering teams, the ability to programmatically access category rankings, product performance metrics, and shop-level data without manual exports is a meaningful operational advantage. The web interface serves as a quick-lookup tool alongside the API.

Key features:

Programmatic access to category rankings, product performance metrics, and shop-level data without manual CSV exports or screenshot workflows

Category-level data including top products by subcategory, shop distribution, and growth rate trends

9. TikTok Seller Center: Free Official Analytics for Your Own Shop

Parameter

Details

Tool name

TikTok Seller Center

Standout feature

First-party data accuracy. Revenue, order, and fulfillment metrics come directly from TikTok's internal systems, not third-party estimates.

Data source

TikTok's own platform data. First-party, verified, no estimation.

Starting price

Free

Free trial/plan

Free for all TikTok Shop sellers

Before spending a dollar on third-party analytics, make sure you are actually using what TikTok gives you for free. Seller Center provides first-party data on orders, revenue, fulfillment performance, and basic advertising metrics. The data is accurate because it comes directly from TikTok's internal systems rather than being estimated by an outside algorithm.

The limitation is obvious: Seller Center shows only your data. You cannot research competitors, discover trending products across the platform, or analyze category-level demand. It is a necessary foundation. It is not a substitute for competitive intelligence.

Key features

Opportunity Center flags high-demand product categories with limited supply, which is TikTok's own signal for where organic traffic support is available

Creator Marketplace for finding and contacting affiliate partners at no additional cost, with filtering by niche and content style

Creative Center surfaces trending hashtags, popular sounds, and content formats gaining traction, useful for content strategy even without paid tools

How to Choose the Right TikTok Shop Analytics Tool

The right tool depends on the specific bottleneck you are trying to solve, not on which platform has the most features.

If you need to understand the market structure before entering a category, SmartScout TikTok Analytics is the only platform building that capability. Register for early access.

If you need to find specific products to sell and identify creators to partner with, Kalodata provides the deepest product and creator data available. The 7-day free trial makes it risk-free to evaluate.

If you run an agency or manage multiple TikTok Shop brands, FastMoss gives you the competitive monitoring infrastructure that agency workflows demand.

If you are an Amazon seller adding TikTok Shop as a new channel, Helium 10 handles the operational logistics of listing conversion and cross-channel profit tracking. But pair it with a TikTok-native research tool for product discovery and competitive intelligence.

If you are testing whether TikTok Shop is worth your time and do not want to spend anything until you know, start with EchoTik's free plan and TikTok's own Seller Center. Upgrade once your revenue justifies the investment.

The Complete TikTok Shop Analytics Stack for 2026

No single tool covers every layer of TikTok Shop intelligence. The sellers and agencies generating the most revenue tend to stack two to three tools that complement each other without overlapping.

Ad creative intelligence: PiPiADS (if you run paid TikTok campaigns)

Own-shop performance: TikTok Seller Center (free, non-negotiable)

For sellers already using SmartScout for Amazon, the TikTok launch means evaluating market opportunities across both platforms from a single provider. That cross-platform view is particularly valuable for brands and agencies deciding how to allocate inventory and advertising budgets between channels.

The Bottom Line

Most TikTok Shop tools answer the same question in slightly different ways: what is selling right now? That question matters, but it is the second question, not the first. A product can be selling well inside a category that is already saturated, controlled by three dominant shops, or about to roll over. Knowing what is hot without knowing the shape of the market around it is how sellers end up entering categories at the exact moment margins collapse.

That is the case for starting with category intelligence. Map the market first, find the niches where demand is outpacing supply, then use product and creator tools to execute inside the categories worth entering. SmartScout TikTok Analytics is being built around that exact sequence, the same way SmartScout already maps Subcategories and brands on the Amazon side. For sellers and agencies running both channels, it means evaluating opportunities across Amazon and TikTok Shop from a single provider instead of stitching together separate tools and separate logic.

If you want to be first in line when the TikTok module launches, register for early access. And if you want to start putting category and market intelligence to work today, every SmartScout plan comes with a 7-day money-back guarantee, so there is no risk in seeing what category-first research does for your sourcing decisions before you commit.

Amazon wanted more people to join Prime, and one big sale day was the cleanest way to do it. This is when Prime Day first began in July 2015 as a one-day birthday promotion.

Eleven events later, it has become something much bigger. The 2025 edition stretched across four days, ran in more than 25 countries, and drove an estimated $24.1 billion in U.S. online spend across every retailer, not just Amazon.

This guide pulls together the most recent Prime Day statistics in one place, with sources you can verify. SmartScout tracks Prime Day closely because the patterns that surface during the event tend to shape seller strategy for the rest of the year.

Key Prime Day Statistics at a Glance

Shoppers in the US spent $24.1 billion online in 2025 across all retailers, up 30.3% year over year

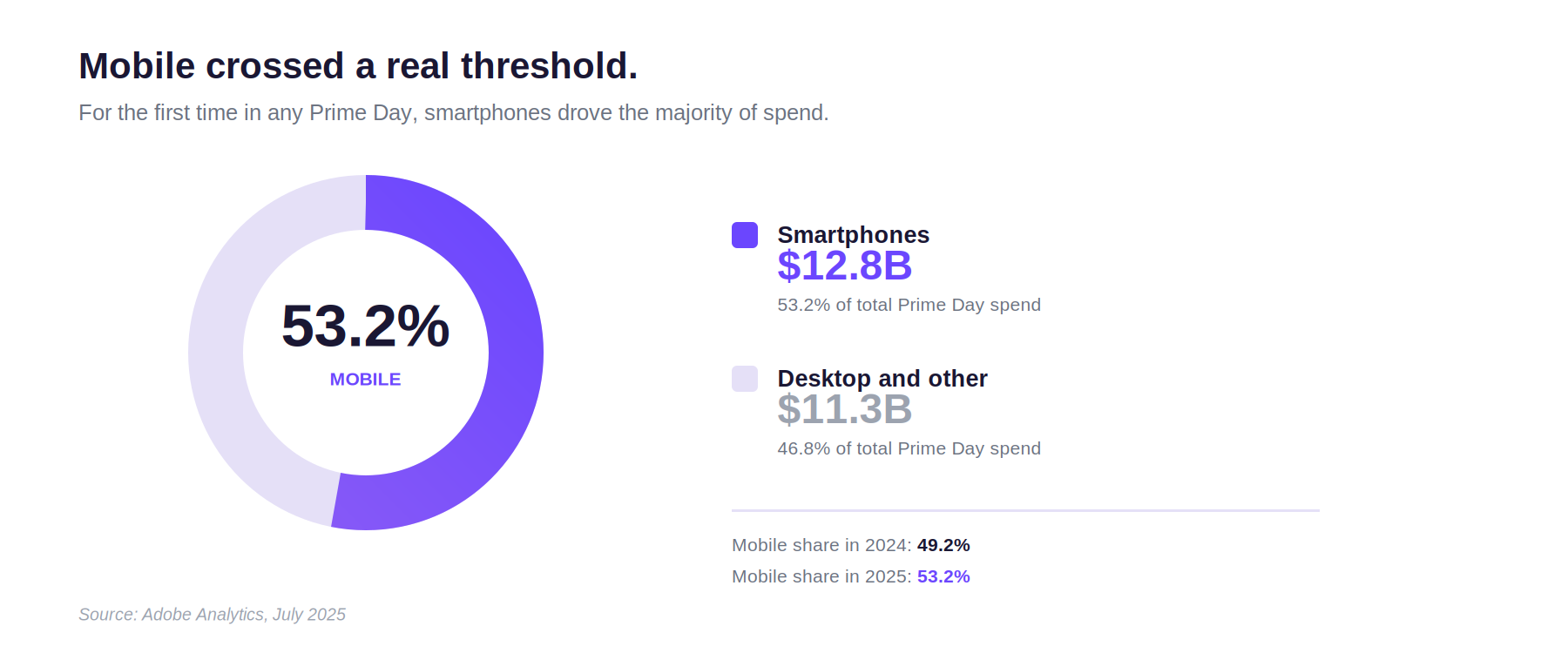

53.2% of transactions happened on mobile devices, with smartphones contributing $12.8 billion in Prime Day Sales 2025

The average order value was $53.34, and the average household spent around $156.37

67% of items sold were priced under $20

Traffic from generative AI tools to U.S. retail sites jumped 3,300% year over year during the Prime Day event

Buy Now, Pay Later orders accounted for a total of 8.1% of all online orders, totaling $2 billion across four days

Amazon Prime Day Sales Statistics

Amazon does not publish Prime Day-specific revenue figures. The numbers below come from third-party analysts, mainly Adobe Analytics for U.S. spend and Statista's compiled series.

Methodologies and geographic coverage differ between sources, so these are estimated numbers rather than exact figures.

Year

Estimated Sales

Notes

2015

$0.9 Billion (global)

First Prime Day, 24-hour event

2019

$7.2 Billion (global)

Expanded to 48 hours

2020

$10.4 Billion (global)

Delayed to October due to COVID-19

2021

$11.2 Billion (global)

Returned to summer

2022

$11.9 Billion (global)

Over 300 million items sold

2023

$12.9 Billion (global) / $12.7B (U.S.)

375 million items sold worldwide

2024

$14.2 Billion (U.S.)

11.7% YoY growth in the U.S.

2025

$24.1 Billion (U.S. ecommerce total)

First four-day event, 30.3% YoY growth

Sources: Statista global series, Statista U.S. series, and Adobe Analytics for 2025. The 2025 figure measures total U.S. retailer online spend during the window, not Amazon-only revenue.

The format change is the single biggest reason 2025's headline number was up 30% year over year. Longer event, more transaction time, more reported revenue. For context, the 2025 four-day total roughly matched the combined 2024 Black Friday and Cyber Monday online sales.

Per-day intensity actually dropped. NielsenIQ's panel data shows the average daily order total in 2025 was 136% above Amazon's year-to-date daily average, versus 247% above the year-to-date daily average in the 2024 two-day event.

So the event is bigger overall, but each individual day is less concentrated than before.

Prime Day Shopper Statistics

About 89% of 2025 Prime Day shoppers said they had shopped a previous Prime Day, and 87% identified as Prime members of more than a year.

A further 96% of shoppers knew it was Prime Day before they shopped, and 52% said Prime Day was their primary reason for visiting Amazon during that period.

Profile Dimension

2025 Snapshot

Typical observed shopper

High-income, suburban female, age 45 to 64

Gender share

Women accounted for a higher share than in H1 2025

Top generations

Gen X and Millennials led shopping share

Income mix

Lower-income shoppers no longer over-indexed (a shift from 2024)

Prime member share

About 87% identified as Prime members of more than a year

Walmart Deals, Target Circle Week, and Best Buy's Black Friday in July all pulled real Prime Day attention. 49% of Prime Day shoppers also shopped Walmart, 38% shopped Target Circle Week, and 11% shopped Best Buy. And 57% of Prime Day shoppers compared Amazon's prices to other retailers before placing orders.

Prime Day Consumer Spending Statistics

The average Prime Day order in 2025 was $53.34, down roughly 8% from $57.97 in 2024. But shoppers placed more separate orders. Roughly 63% of households placed two or more, which pushed average household spend up to $156.37, a 2.6% bump from $152.33 the prior year.

Here is how that broke down by order size and order count:

The pattern is clear once you see the per-item average. Spend per item dropped to $24.59 in 2025 from $28.47 at the same point in 2024. More orders, cheaper items. This was a stock-up event, not a splurge event.

BNPL hit a new high in 2025. It accounted for 8.1% of online orders, up from 7.4% the year before, and totaled $2 billion in spend across the four days, growing 33.3% year over year. Adobe's survey respondents reached for BNPL most often in apparel, electronics, home goods, and health and beauty.

Most Popular Prime Day Categories

Numerator's verified-buyer survey ranked the most-purchased categories. Everyday essentials dominate the leaderboard:

Category

Share of Prime Day Buyers

Household Essentials

30%

Apparel & Shoes

30%

Home Goods (bedding, décor)

27%

Health & Wellness

26%

Beauty & Cosmetics

25%

Consumer Electronics

19%

Pet Products

15%

Groceries

15%

Toys & Video Games

12%

Source: Numerator 2025 Prime Day Survey.

Biggest category lifts on Prime Day

Adobe measures category lift differently. It compares Prime Day sales against the daily average from June 2025, which surfaces where Prime Day pulled in disproportionate demand:

Category

Lift vs. June 2025 Daily Average

Kids’ apparel

+250%

Home security

+185%

School supplies

+175%

Refrigerators and freezers

+160%

Headphones and speakers

+155%

Appliances (broad)

+112%

Office supplies

+105%

Electronics (broad)

+95%

Books

+81%

Source: Adobe Analytics, Prime Day 2025.

Mobile Shopping & Ecommerce Trends

For the first time in any Prime Day, mobile revenue beat desktop revenue. Smartphones generated 53.2% of online sales, roughly $12.8 billion in spending. The 2024 share was 49.2%, so this is not a small jump. It is a structural shift.

Mobile is now the primary driver of e-commerce sales overall, which has real consequences for how sellers should design listings and ads. Mobile-first product imagery, A+ content that renders on small screens, and ads optimized for thumb scrolling all matter more than they did a year ago.

Prime Day Seller Statistics

Most coverage of Prime Day focuses on what consumers did. The seller side often matters more for strategy. Ad costs, conversion rates, and inventory positioning shape outcomes that the GMV number cannot show.

Ad spend and CPC trends

Skai called Prime Day 2025 the biggest Prime Day in Amazon Ads history, though year-over-year ad spend growth was slower than in prior years. Across Skai's client base, daily averages outperformed the 30-day baseline.

Clicks were up 108%, impressions up 114%, click-through rate climbed, and cost-per-click actually fell. That pattern says advertisers paced their budget across all four days instead of front-loading day one.

Metric

Prime Day 2025 vs. 2024

Sponsored Products CPC

Down ~11% YoY

Clicks vs. 30-day baseline

Up 108%

Impressions vs. 30-day baseline

Up 114%

Click-through rate

Higher than 2024

ROAS (one agency benchmark)

~$4.59, up 12.8% YoY

Day 1 share of attributed sales

34%

Day 3 share of attributed sales

19% (lowest)

Halo effects beyond direct deals

Even brands that did not run formal Prime Day deals saw a sales lift. Acadia's data shows roughly a 46% lift versus their normal weekly baseline during the event. That changes the question for many sellers from "should we run a deal" to "are our listings, inventory, and ads ready for the surge either way?"

How two brands used Prime Day differently

The 46% halo lift tells one side of the story. The other side is what happens when brands actively run deals, and how much the execution varies even among large sellers. SmartScout's marketplace data from July 2025 shows two brands that both treated Prime Day as a growth lever but pulled it in opposite directions.

Prime Day 2026 timing has compressed seller prep

Prime Day 2026 is expected in late June rather than mid-July, with industry sources pointing to roughly June 23 to 25. Deal submissions are expected to open in late March and close on May 26. For sellers who used to treat July as a soft prep target, the calendar has shifted by about a month. Inventory and ad planning should start in March, not June.

Prime Day Pricing & Discount Statistics

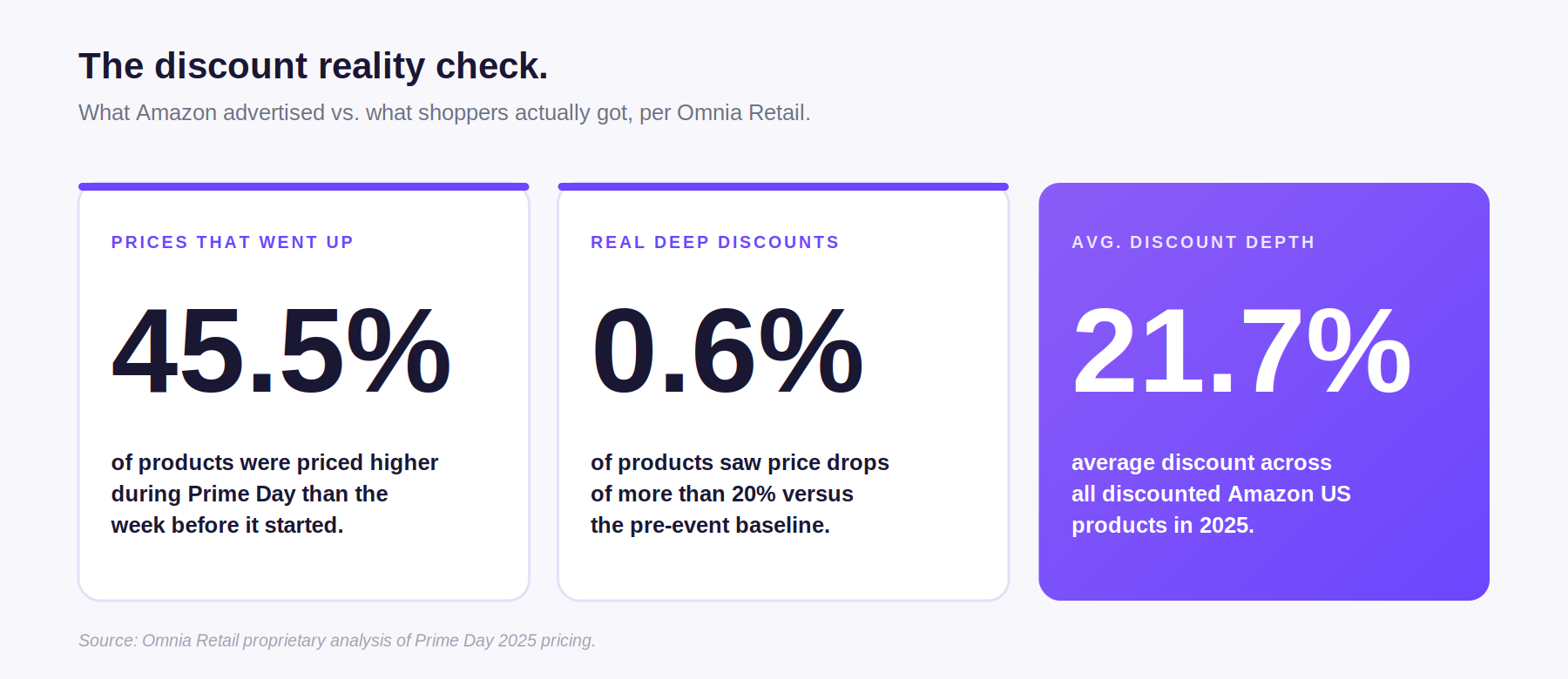

This is the section that gets the least attention in most Prime Day roundups, which is exactly why it matters. Omnia Retail's proprietary analysis found that the overall average discount depth across discounted Amazon US products in 2025 was around 21.7%.

Amazon's own tech brands like Fire TV, Echo, Kindle, and Ring averaged about 30% off, and Amazon Private Brands ran up to 40% off. For third-party products, the picture was more complicated.

Omnia's most striking finding: 45.5% of products were priced higher during Prime Day 2025 than the week before the event. Only 0.6% of products saw price reductions of more than 20% from the pre-event baseline. For most listings, the "Prime Day discount" reverted prices to where they had been a month earlier, instead of offering a genuinely new low.

Adobe's view shows higher peak discounts

Both views can be accurate at the same time. Adobe measures peak discount depth against listed prices, not pre-event street prices. By that view, here is how the major categories landed:

Category

Peak Discount 2025

Peak Discount 2024

Apparel

24%

20%

Electronics

23%

23%

Toys

19%

15%

Televisions

18%

16%

Appliances

17%

14%

Furniture

16%

16%

Computers

13%

11%

Sporting goods

11%

11%

Source: Adobe Analytics, Prime Day 2025 (Adobe).